Markets in a Minute

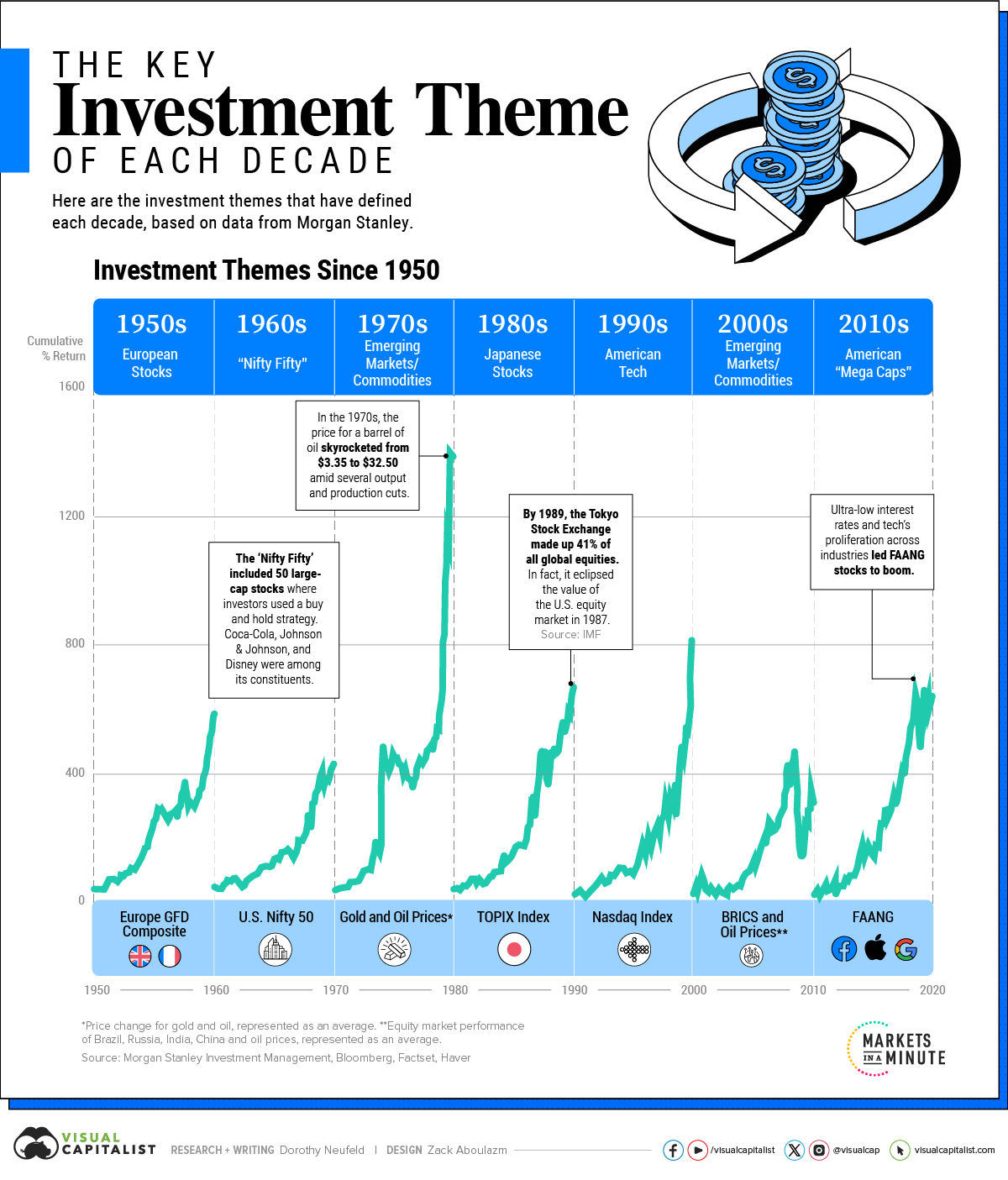

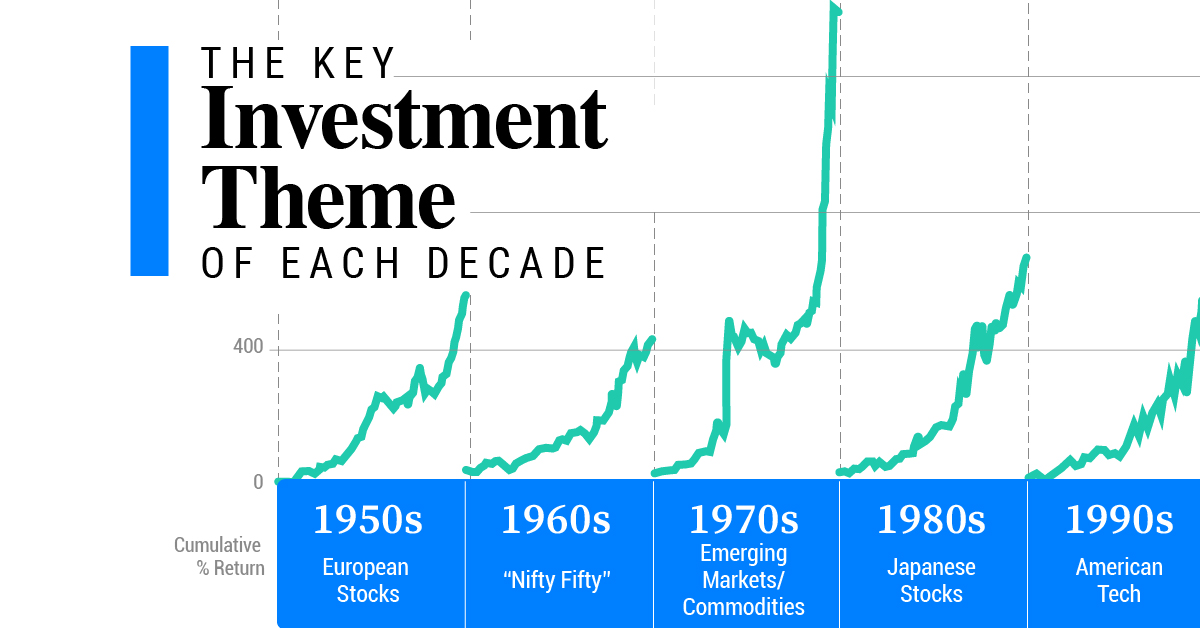

Charted: The Key Investment Theme of Each Decade (1950-Today)

Visualizing the Key Investment Theme of Each Decade

Over modern history, a key investment theme has broadly characterized each decade.

In each case, a particular asset class, sector, or region captivated investors for an extended period, driving returns and outperforming the rest of the market.

This graphic shows 70 years of key investment themes, based on analysis from Ruchir Sharma of Morgan Stanley Investment Management via NS Capital.

Investment Themes by Decade

These decade-defining themes are often the product of a confluence of factors, including the macroeconomic environment, geopolitics, monetary policy, or other structural shifts like technological disruption.

Here are the central investment themes since the 1950s, each with at least 400% cumulative returns over each period:

| Decade | Investment Theme | Index / Asset |

|---|---|---|

| 1950s | European Stocks | Europe GFD Composite |

| 1960s | “Nifty Fifty” Stocks | U.S. Nifty 50 |

| 1970s | Emerging Markets / Commodities | Gold and Oil Prices* |

| 1980s | Japanese Stocks | TOPIX Index |

| 1990s | American Tech | Nasdaq Index |

| 2000s | Emerging Markets / Commodities | BRICs and Oil Prices** |

| 2010s | American “Mega Caps” | FAANG |

*Price change for gold and oil, represented as an average. **Equity market performance of Brazil, Russia, India, China and oil prices, represented as an average.

The 1950s saw a boom in European stocks during the post-war recovery. This was fueled by significant investment from corporations and governments as Europe became more integrated.

Then in the 1960s, investors poured into blue chip stocks in the “Nifty Fifty” including Johnson & Johnson, Disney, and Coca-Cola. The main premise was that these strong franchises would deliver high returns over the long run. During the 1973-1974 bear market, shares cratered.

As oil skyrocketed from $3.35 to $32.50 through the 1970s amid production and output cuts, commodities dominated, along with emerging economy exporters of oil and gold.

Later, through the 1980s, Japanese stocks dramatically increased. In 1989, the Tokyo Stock Exchange made up 41% of all global equities. It had eclipsed the value of the U.S. equity market just two years earlier.

In part owing to strong U.S. economic growth, American tech stocks flourished through the 1990s. While many high-flying tech stocks were wiped out during the crash in 2000, some still remain today. Qualcomm, which jumped 2,620% in 1999, is a multi-billion dollar semiconductor company. Amazon and Cisco were other survivors of this era.

Pivoting from growth assets, investors returned to commodities and emerging markets over the 2000s, this time with BRIC economies—Brazil, Russia, India, and China. The 2010s saw the rise of FAANG stocks as tech proliferated across countless industries.

The Next Decade Ahead

Given how each decade seems to be defined by a key investment theme, Sharma suggests that it won’t be another driven defined by American stocks.

The disconnect between the size of U.S. equity markets, at 43% of the global share, and its economic output, which is 26% of the world’s total, is one reason driving a new shift.

Another factor is stark differences in valuations. Today, the U.S. stock market compared to the rest of the world is at its highest relative level in 100 years, suggesting it is overvalued and primed for a shift.

Whether global stocks gain a greater global equity market share—to become a key investment cycle of this decade—remains an open question.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022