Markets in a Minute

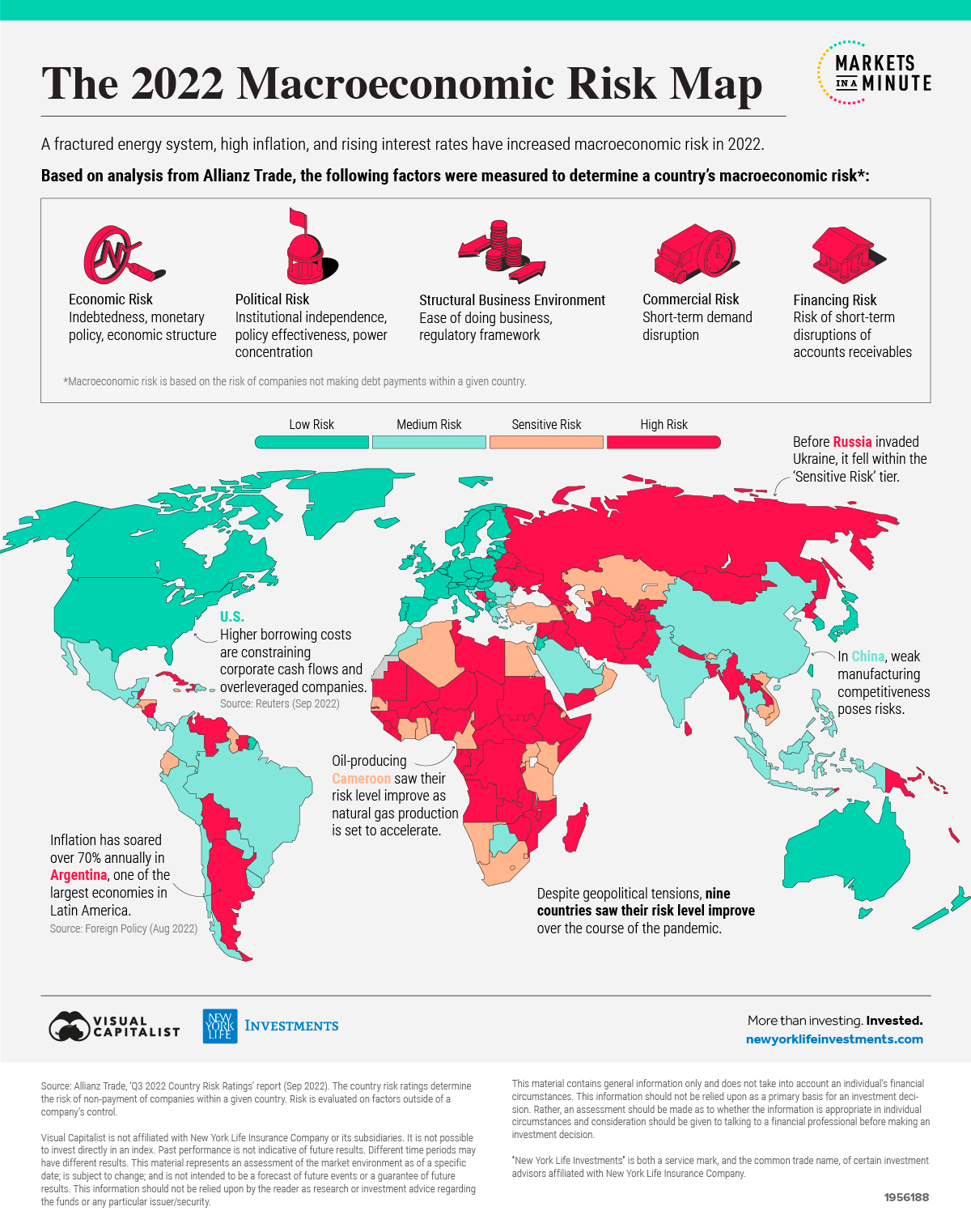

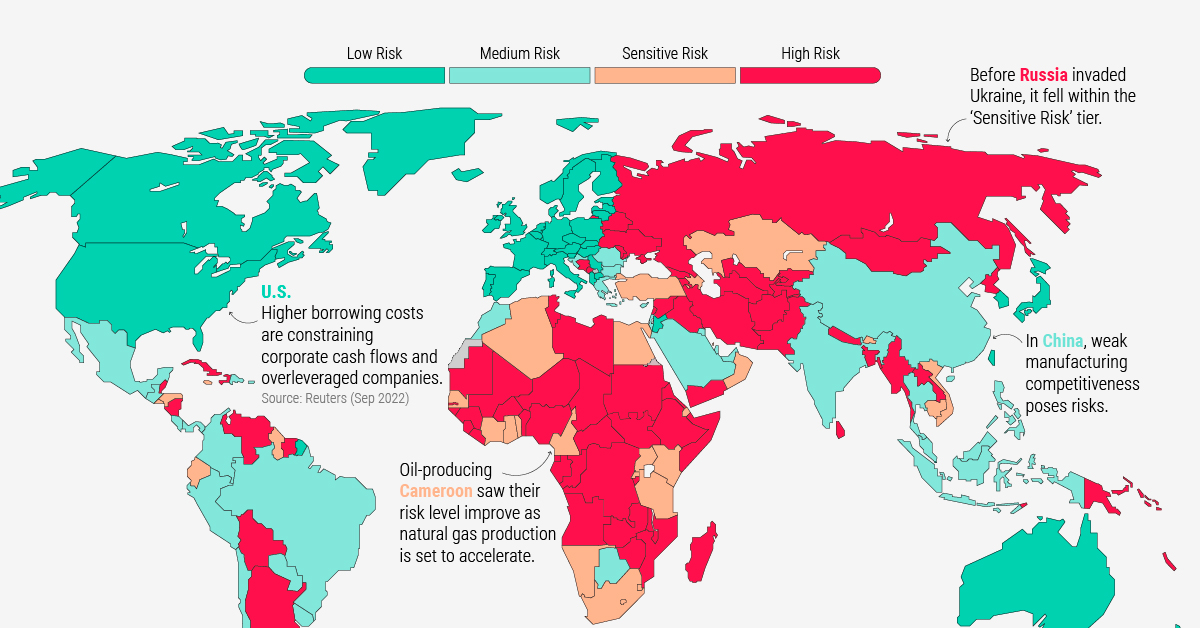

Mapped: Global Macroeconomic Risk, by Country in 2022

This infographic is available as a poster.

This infographic is available as a poster.

The Global Macroeconomic Risk Map in 2022

When Russia invaded Ukraine, vital grain export routes shut down in Ukraine’s Port of Odesa—causing global food prices to soar.

Since then, energy markets have been disrupted, leading European heating costs to skyrocket. Meanwhile, global inflation is high, and central banks around the world are raising interest rates in response to rising price pressures.

This Markets in a Minute from New York Life Investments shows the world macroeconomic risk map in 2022 against a shifting economic landscape.

Macroeconomic Risk Map: The Methodology

Macroeconomic risk is an overarching metric that takes into account many external risk factors that could impact investor portfolios and business valuations within a country. These factors include items like monetary policy, trade flows, and the political climate.

In the data from Allianz Trade, a country’s macroeconomic risk is determined based on the following categories:

- Economic Risk: Indebtedness, monetary policy, economic structure

- Political Risk: Institutional independence, policy effectiveness, power concentration

- Structural Business Environment: Ease of doing business, regulatory framework

- Commercial Risk: Short-term demand disruption

- Financing Risk: Risk of short-term disruptions of accounts receivables

In the context of this data, each calculation for macroeconomic risk level is ultimately a proxy representing the risk of companies not making debt payments within a given country.

Increasing Challenges

After the U.S. increased interest rates in the 1980s, many emerging markets fell into crisis as debt payments (denominated in U.S. dollars) rose. Fast forward 10 years later, and rising U.S. interest rates triggered the Mexican peso crisis in 1994.

More recently, in 2013, when the Fed began tapering its bond purchases, it led to steep investment outflows from India, Indonesia, and Brazil.

Today, as U.S. interest rates rise at the fastest pace in decades, emerging markets are facing new pressures. The good news is that some countries are absorbing the shock thanks to higher bank reserves and reasonable growth. However, at the same time, high inflation and social unrest are fueling higher risk.

Given this complex picture, which countries and jurisdictions are at the highest risk as geopolitical tensions unfold?

| Country | Risk Level |

|---|---|

| 🇦🇫 Afghanistan | High Risk |

| 🇦🇱 Albania | High Risk |

| 🇦🇴 Angola | High Risk |

| 🇦🇷 Argentina | High Risk |

| 🇦🇲 Armenia | High Risk |

| 🇧🇩 Bangladesh | High Risk |

| 🇧🇧 Barbados | High Risk |

| 🇧🇾 Belarus | High Risk |

| 🇧🇿 Belize | High Risk |

| 🇧🇴 Bolivia | High Risk |

| 🇧🇦 Bosnia and Herzegovina | High Risk |

| 🇧🇫 Burkina Faso | High Risk |

| 🇧🇮 Burundi | High Risk |

| 🇨🇫 Central African Republic | High Risk |

| 🇹🇩 Chad | High Risk |

| 🇰🇲 Comoros | High Risk |

| 🇨🇩 Congo (Democratic Rep Of) | High Risk |

| 🇨🇬 Congo (People's Rep Of) | High Risk |

| 🇨🇺 Cuba | High Risk |

| 🇬🇶 Equatorial Guinea | High Risk |

| 🇪🇷 Eritrea | High Risk |

| 🇪🇹 Ethiopia | High Risk |

| 🇫🇯 Fiji | High Risk |

| 🇬🇦 Gabon | High Risk |

| 🇬🇲 Gambia | High Risk |

| 🇬🇪 Georgia | High Risk |

| 🇬🇳 Republic of Guinea | High Risk |

| 🇬🇼 Guinea Bissau | High Risk |

| 🇭🇹 Haiti | High Risk |

| 🇮🇷 Iran | High Risk |

| 🇮🇶 Iraq | High Risk |

| 🇰🇿 Kazakhstan | High Risk |

| 🇰🇬 Kyrgyzstan | High Risk |

| 🇱🇦 Laos | High Risk |

| 🇱🇧 Lebanon | High Risk |

| 🇱🇷 Liberia | High Risk |

| 🇱🇾 Libya | High Risk |

| 🇲🇬 Madagascar | High Risk |

| 🇲🇼 Malawi | High Risk |

| 🇲🇻 Maldives | High Risk |

| 🇲🇱 Mali | High Risk |

| 🇲🇭 Marshall Islands | High Risk |

| 🇲🇷 Mauritania | High Risk |

| 🇲🇩 Moldova | High Risk |

| 🇲🇳 Mongolia | High Risk |

| 🇲🇪 Montenegro | High Risk |

| 🇲🇿 Mozambique | High Risk |

| 🇲🇲 Myanmar (Burma) | High Risk |

| 🇳🇷 Nauru | High Risk |

| 🇳🇵 Nepal | High Risk |

| 🇳🇮 Nicaragua | High Risk |

| 🇳🇪 Niger | High Risk |

| 🇳🇬 Nigeria | High Risk |

| 🇰🇵 North Korea | High Risk |

| 🇵🇰 Pakistan | High Risk |

| 🇵🇬 Papua New Guinea | High Risk |

| 🇷🇺 Russia | High Risk |

| 🇸🇨 Seychelles | High Risk |

| 🇸🇱 Sierra Leone | High Risk |

| 🇸🇧 Solomon Islands | High Risk |

| 🇸🇴 Somalia | High Risk |

| 🇸🇸 South Sudan | High Risk |

| 🇱🇰 Sri Lanka | High Risk |

| 🇸🇩 Sudan | High Risk |

| 🇸🇷 Suriname | High Risk |

| 🇸🇾 Syria | High Risk |

| 🇹🇯 Tajikistan | High Risk |

| 🇹🇱 Timor Leste | High Risk |

| 🇹🇬 Togo | High Risk |

| 🇹🇴 Tonga | High Risk |

| 🇹🇳 Tunisia | High Risk |

| 🇹🇲 Turkmenistan | High Risk |

| 🇺🇦 Ukraine | High Risk |

| 🇺🇿 Uzbekistan | High Risk |

| 🇻🇪 Venezuela | High Risk |

| 🇾🇪 Yemen | High Risk |

| 🇿🇲 Zambia | High Risk |

| 🇿🇼 Zimbabwe | High Risk |

Authoritarian rule has gripped Afghanistan, with the Taliban seeing its one-year anniversary of rule. Argentina, also at high risk, faces over 70% annual increases in inflation which could rise as much as 100% by year-end.

After the invasion of Ukraine, Russia’s risk was moved to the highest level. Despite sweeping sanctions across the ninth-largest economy in the world, GDP is projected to fall -3.4%.

Weathering the Storm

Despite often facing their own challenges, many countries continue to be deemed to have low macroeconomic risk. Several of these are in Europe, Asia, and smaller island jurisdictions, in addition to North America.

| Country | Risk Level |

|---|---|

| 🇦🇸 American Samoa | Low Risk |

| 🇦🇩 Andorra | Low Risk |

| 🇦🇶 Antarctica | Low Risk |

| 🇦🇺 Australia | Low Risk |

| 🇦🇹 Austria | Low Risk |

| 🇧🇪 Belgium | Low Risk |

| 🇧🇲 Bermuda | Low Risk |

| 🇻🇬 British Virgin Islands | Low Risk |

| 🇨🇦 Canada | Low Risk |

| 🇧🇶 Caribbean Netherlands | Low Risk |

| 🇰🇾 Cayman Islands | Low Risk |

| 🇨🇽 Christmas Island | Low Risk |

| 🇨🇨 Cocos (Keeling) Islands | Low Risk |

| 🇨🇿 Czech Republic | Low Risk |

| 🇩🇰 Denmark | Low Risk |

| 🇪🇪 Estonia | Low Risk |

| 🇫🇰 Falkland Islands | Low Risk |

| 🇫🇴 Faroe Islands | Low Risk |

| 🇫🇮 Finland | Low Risk |

| 🇬🇫 French Guiana | Low Risk |

| 🇫🇷 France | Low Risk |

| 🇹🇫 French Southern Territory | Low Risk |

| 🇩🇪 Germany | Low Risk |

| 🇬🇮 Gibraltar | Low Risk |

| 🇬🇱 Greenland | Low Risk |

| 🇬🇵 Guadeloupe | Low Risk |

| 🇬🇺 Guam | Low Risk |

| 🇭🇲 Heard and McDonald Islands | Low Risk |

| 🇮🇪 Ireland | Low Risk |

| 🇮🇹 Italy | Low Risk |

| 🇯🇵 Japan | Low Risk |

| 🇱🇻 Latvia | Low Risk |

| 🇱🇮 Liechtenstein | Low Risk |

| 🇱🇹 Lithuania | Low Risk |

| 🇱🇺 Luxembourg | Low Risk |

| 🇲🇹 Malta | Low Risk |

| 🇲🇨 Monaco | Low Risk |

| 🇲🇶 Martinique | Low Risk |

| 🇾🇹 Mayotte | Low Risk |

| 🇳🇱 Netherlands | Low Risk |

| 🇳🇨 New Caledonia | Low Risk |

| 🇳🇿 New Zealand | Low Risk |

| 🇳🇫 Norfolk Island | Low Risk |

| 🇲🇵 Northern Mariana Islands | Low Risk |

| 🇳🇴 Norway | Low Risk |

| 🇵🇳 Pitcairn Islands | Low Risk |

| 🇷🇪 Reunion | Low Risk |

| 🇸🇲 San Marino | Low Risk |

| 🇸🇬 Singapore | Low Risk |

| 🇸🇰 Slovakia | Low Risk |

| 🇬🇸 South Georgia/Sandwich Islands | Low Risk |

| 🇰🇷 South Korea | Low Risk |

| 🇪🇸 Spain | Low Risk |

| 🇸🇭 St Helena | Low Risk |

| 🇵🇲 St. Pierre Et Miquelon | Low Risk |

| 🇸🇯 Svalbard & Jan Mayen | Low Risk |

| 🇸🇪 Sweden | Low Risk |

| 🇨🇭 Switzerland | Low Risk |

| 🇹🇼 Taiwan | Low Risk |

| 🇹🇰 Tokelau | Low Risk |

| 🇹🇨 Turks & Caicos | Low Risk |

| 🇬🇧 United Kingdom | Low Risk |

| 🇺🇸 United States | Low Risk |

| 🇻🇮 U.S. Virgin Islands | Low Risk |

| 🇻🇦 Vatican City | Low Risk |

| 🇼🇫 Wallis & Futuna | Low Risk |

Although Taiwan faces increased tensions with China, risk remains low due to strong institutions and a stable multiparty democracy. Still, China’s aim to govern the country could intensify and become more explicit.

Additionally, the United Kingdom has faced growing market instability after bold tax-cut announcements which were later abandoned. Investors have grown uneasy, illustrated by the fall in the sterling and rising gilt yields, the yields on their government bonds.

In the U.S., rising interest rates could likely place added risk on corporate debt.

Today, U.S. corporate debt stands at 80% of GDP, up from 67% in 2007. Roughly a third of this debt falls within the lowest investment-grade level, BBB. However, reforms that followed the Global Financial Crisis required banks to follow stricter capital requirements, which has put regulated institutions in a stronger position to withstand market turmoil.

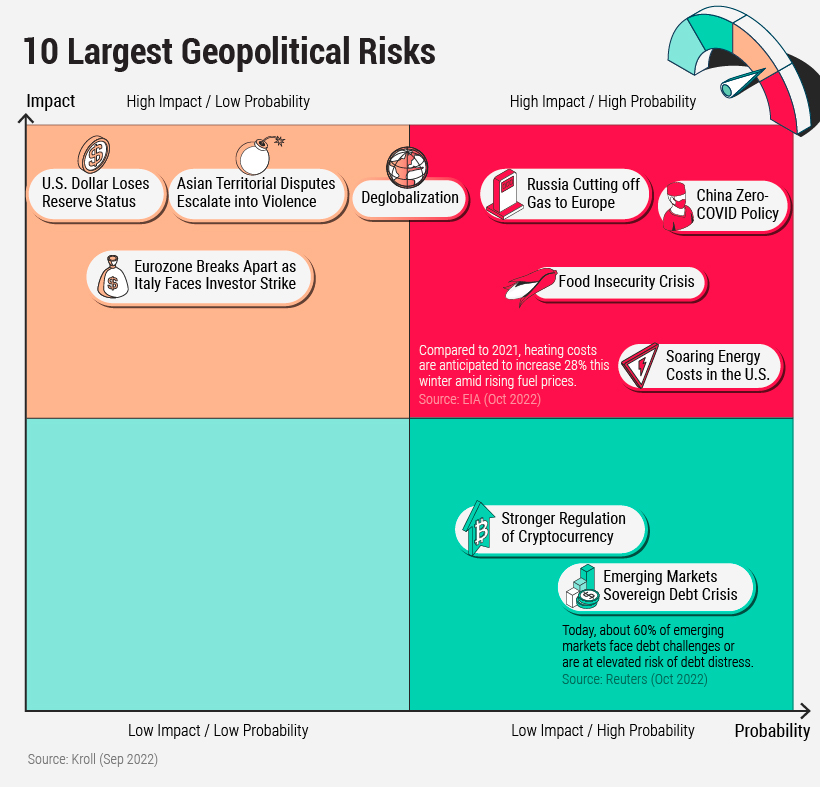

Future Risks

With these factors in mind, the chart below looks at the top 10 geopolitical risks looking ahead, according to risk consulting firm Kroll.

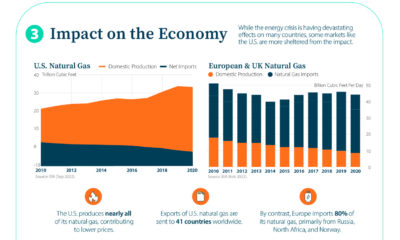

The risk of Russia entirely cutting off gas supplies to Europe could present increasing challenges, especially into 2023 and 2024. This year, Russia’s gas supplies to Europe have reduced by half, causing energy prices to hit record highs. The energy crunch has precipitated corporate bailouts, including one of the highest in Germany’s history.

Global food insecurity could also accelerate if a supply crunch worsens. Russia and Ukraine supply 10% of the world’s calories and provide 26 countries with at least half of their grain products.

Another potential risk is the trend towards deglobalization. While this can be difficult to measure, some data points towards this shift. Over the past few years, world trade to GDP has stagnated after rising for several decades.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators