Markets in a Minute

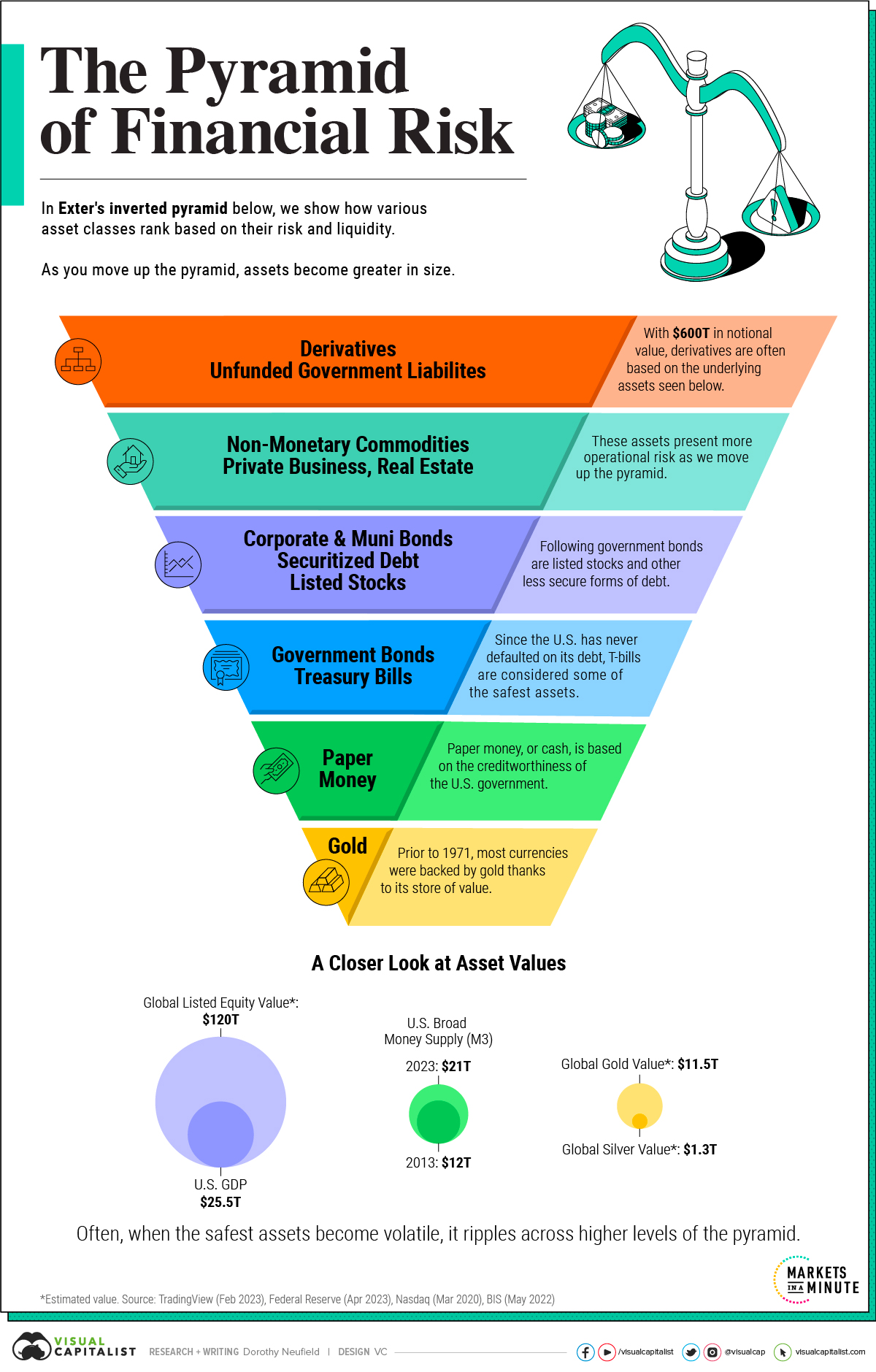

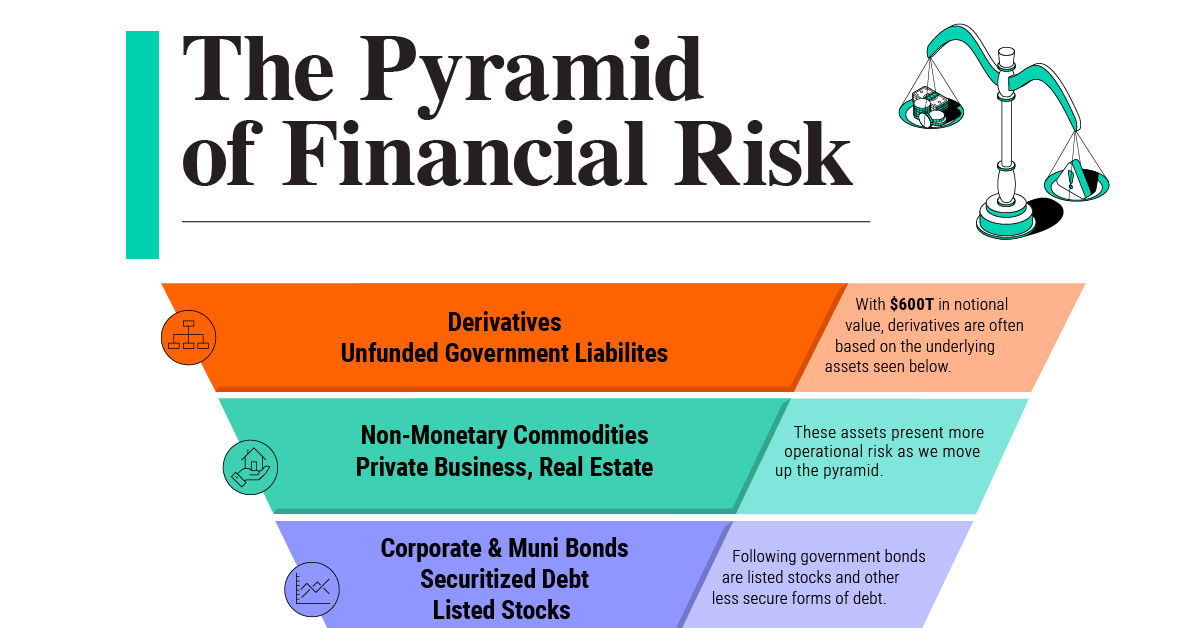

Visualizing the Pyramid of Financial Risk

Visualizing the Pyramid of Financial Risk

Financial risk falls under the limelight during market stress.

In periods of uncertainty, liquidity becomes especially valuable to investors. Assets that are more liquid are convertible into cash without losing much of their value. Consider how investors often flock to U.S. government bonds during economic turmoil thanks to their relative safety.

In the above graphic, we show how assets become both riskier and greater in size by dollar value as they move up Exter’s pyramid, using an adapted model from TradingView.

The Anatomy of Financial Risk

John Exter, an economist and former member of the Federal Reserve, developed the model of financial risk in the mid-1970s.

While he is most known for this inverted pyramid, he also was a founding governor of the Central Bank of Sri Lanka and was an advisor to Paul Volcker when he was chair of the Fed.

In the table below, some of the riskiest assets are derivatives. These are financial instruments based on the movements of an underlying security, such as currencies or commodities. They are often highly leveraged, meaning investors put very little money down to make these wagers, and in turn, can generate losses quickly.

Derivatives have a stunning $600 trillion in notional market value.

| Asset Type | Estimated Global Value Unless Otherwise Indicated |

|---|---|

| 💹 Derivatives* | $600T |

| 🏦 Unfunded Government Liabilities | $93.1T (U.S.) |

| 🛢️ Non-Monetary Commodities | $300T |

| 👔 Private Business | $22T (U.S.) |

| 🏠Real Estate | $326T |

| 💼 Corporate & Municipal Bonds | $14.3T (U.S.) |

| 🏘 Securitized Debt | $1.6T (U.S.) |

| 📈Listed Stocks | $120T |

| 🏛 Government Bonds | $128.3T |

| 📃Treasury Bills | $24.3T |

| 💵 Paper Money** | $8.3T (U.S.) |

| 🧈 Gold | $11.5T |

*Represents notional value, the total value of the underlying contract. **Paper Money represents tangible currency including coins and bank notes. Gold is based on a spot price of $1,750 per oz and 205,238 tonnes. Unfunded government liabilities are debt obligations that have insufficient funds to pay for them.

Private business and real estate are also considered to have higher financial risk. Since there is no central marketplace where they can be sold quickly, they present higher operational risk and lower liquidity. Often, they are more difficult to convert into cash.

Moving down the pyramid are the $120 trillion in listed stocks, which have a centralized market, can trade in significant volumes, and disclose financials while adhering to securities regulations.

U.S. government bonds are considered to have some of the least financial risk globally, thanks to the U.S. never having defaulted on its debt, and the U.S. dollar’s role as a reserve currency. Short-term Treasuries are considered safer than longer-term bonds since they have a lower chance of default given the shorter holding period.

In the event of a liquidity squeeze, many consider cash to be king. Yet to Exter, gold was the safest asset thanks to its finite supply. Prior to 1971, most currencies were pegged to gold. In fact, the current era of fiat money—currencies that are not backed by a physical commodity—is a historical exception.

Domino Effects

During a market crisis, assets at the top of the pyramid tend to have the largest drops in value.

In this way, the degree of loss generally gets smaller the lower down you go in the pyramid. Relatively safer assets may rise in value due to higher demand. Here’s an example from the 2020 market crash that shows how asset classes responded:

| Asset | Price Change (Jan 1 2020-Mar 21 2020) |

|---|---|

| U.S. Oil Index | -61.4% |

| SPDR S&P 500 ETF Trust | -29.5% |

| iShares 20+ Year Treasury Bond ETF | 18.0% |

| S&P U.S. Ultra Short Treasury Bill & Bond Index | 0.8% |

| SPDR Gold Shares ETF | -1.3% |

Source: Nasdaq (Mar 2020), S&P Global (May 2023)

As we can see in the table above, oil fell over 60% as uncertainty increased. Demand for oil typically falls during a weaker economy. By contrast, longer-dated bonds jumped in price.

It’s worth noting that the returns didn’t perfectly follow of the order of the pyramid, but the model can serve as a general guideline for how assets may respond to crisis.

Financial Risk in Today’s Environment

The recent U.S. banking turmoil spurred volatility in some financial assets.

Just as U.S. Treasuries saw extreme volatility since interest rate spikes led them to fall in value, U.S. bonds faced market turbulence. In this way, when safer assets experience uncertainty it can impact levels above in the pyramid.

Interestingly, volatility in bond markets has been higher than volatility in the S&P 500. This can be seen in the difference between the bond market volatility index, known as the MOVE Index, and the VIX Index, which tracks S&P 500 volatility. In April 2023, the difference between the MOVE Index and the VIX Index was near 20-year highs.

What this could point towards is that stocks have become mispriced relative to their true value. As interest rates rise to 16-year highs, borrowing costs have risen and this has hit corporate cash buffers and liquidity.

Overall, how current volatility impacts broader financial risk in the market could take time to materialize. Historically, it has taken roughly 18 months to two years for the true impact of monetary policy to filter through the market.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022