Markets in a Minute

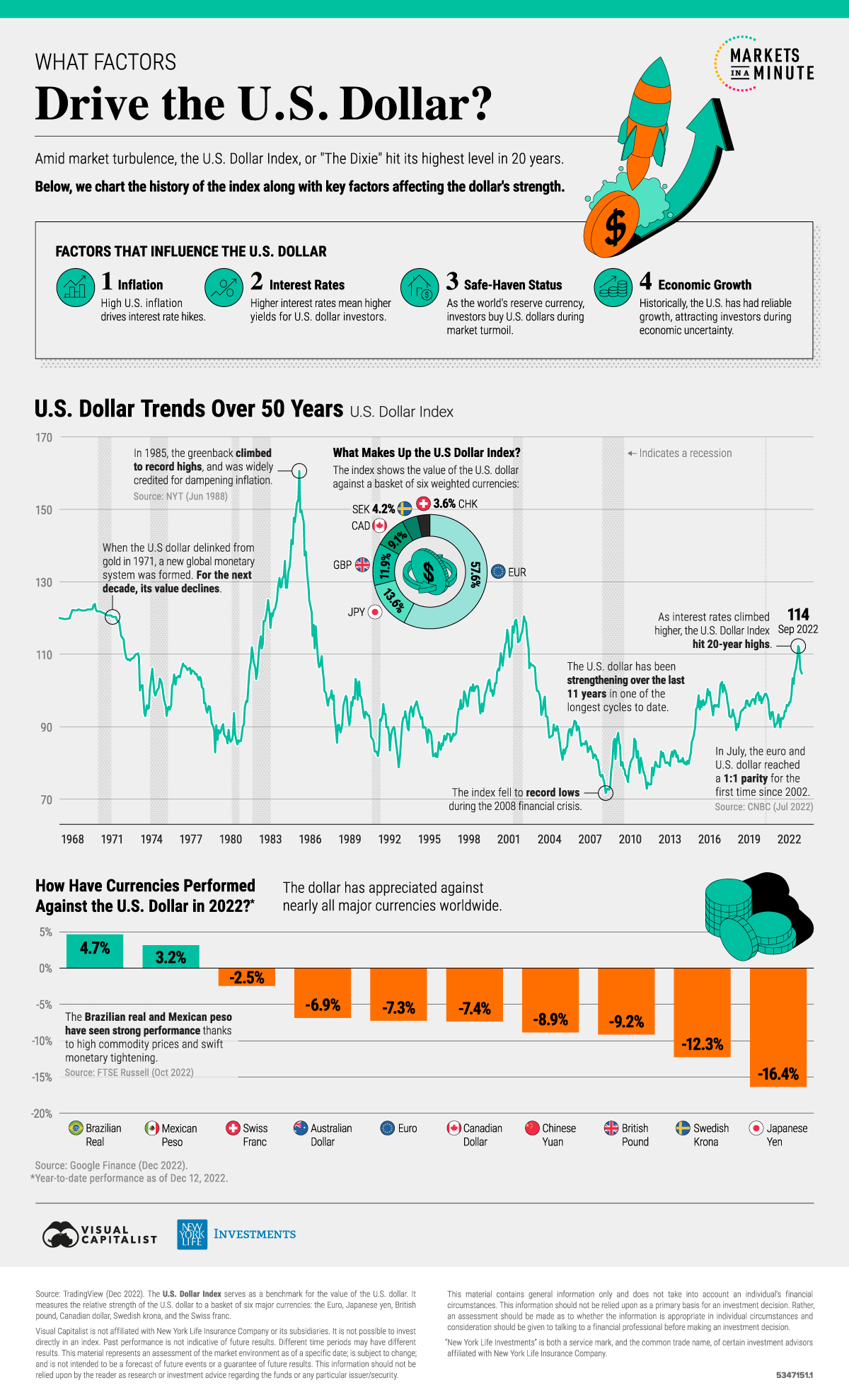

Visualized: What Factors Drive the U.S. Dollar?

This infographic is available as a poster.

This infographic is available as a poster.

What Factors Drive the U.S. Dollar?

In 2022, the U.S. dollar hit 20-year highs as inflation and interest rates rose sharply.

Not only did investors buy U.S. dollars given its role as the world’s reserve currency, but demand for U.S. dollars increased as rising interest rates drove higher returns for the safe-haven currency.

Now, as inflation appears to be easing and lower rate hikes look to be in the cards, the U.S. dollar is cooling. Still, relative to many of the other major global currencies it remains strong.

In the above Markets in a Minute from New York Life Investments, we look at factors that influence the U.S. dollar’s value, and the implications for financial markets and investors.

What Drives the U.S. Dollar?

Importantly, the value of the U.S. dollar is driven by supply and demand factors. During periods of economic uncertainty, investors turn to U.S. dollars because of the underlying strength of the U.S. economy and its role in global financial markets.

Here is a brief overview of some of the key variables that impact the dollar:

| 1. Inflation | 2. Interest Rates | 3. Safe-Haven Status | 4. Economic Growth |

|---|---|---|---|

| High U.S. inflation drives Fed rate hikes. | Higher interest rates mean higher yields for U.S. dollar investors. | Investors turn to U.S. dollars during market turmoil. | Historically, the U.S. has had reliable growth. |

When U.S. inflation is increasing, it has knock-on effects on interest rates. As the Federal Reserve raises interest rates to fight inflation, it makes the returns of holding the greenback more attractive. This is because global investors look to currencies that generate a higher relative return, accounting for other factors.

Meanwhile, the dollar remains the global reserve currency. Today, roughly half of global trade invoices are in U.S. dollars. Many global corporations and governments borrow in U.S. dollars, while revenues are generated in their local currency.

Alongside this, the liquidity and depth of U.S. financial markets are unmatched. In 2022, 59% of central bank reserves were held in U.S. dollars, indicating strong demand internationally.

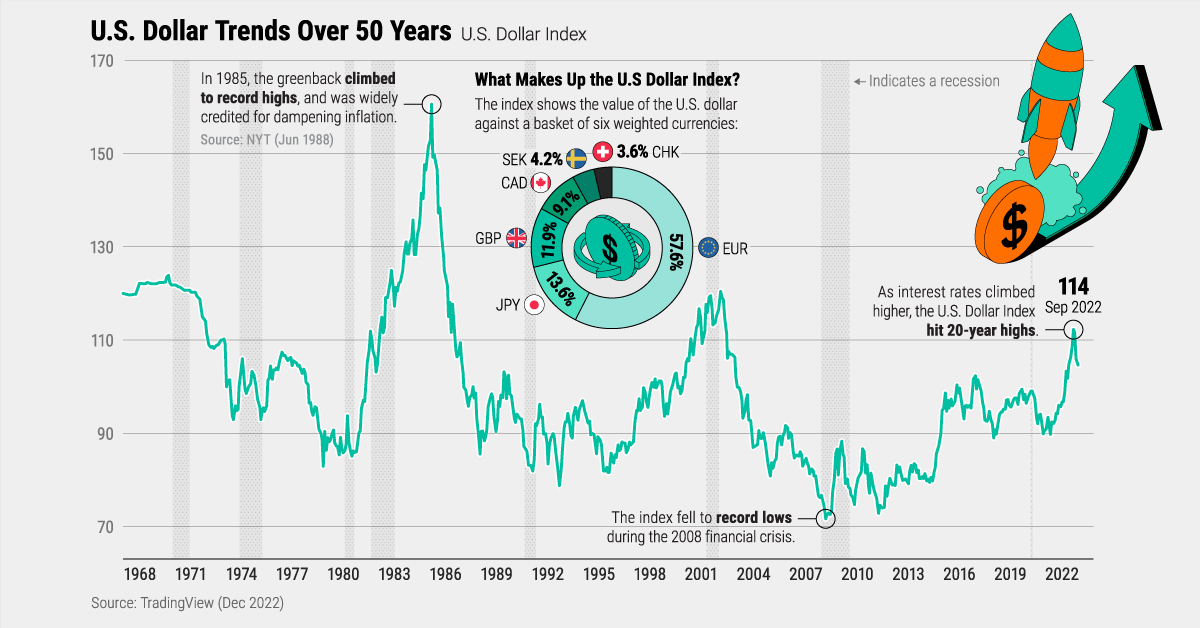

U.S. Dollar Trends Over 50 Years

Since the early 1970s when the U.S. dollar delinked from gold, the currency has had three cycles of strength and three weakening cycles.

These trends can be shown through the U.S. Dollar Index or “Dixie” which tracks the value of the dollar against a basket of weighted currencies.

| U.S. Dollar Cycles | U.S. Dollar Index Peak | Year | Annual Inflation Rate | Annual Interest Rate |

|---|---|---|---|---|

| 1980s | 128 | 1985 | 3.6% | 8.1% |

| 1990s - 2000s | 113 | 2002 | 1.6% | 1.7% |

| 2011 - 2020s | 114 | 2022 | 7.1% | 4.0% |

Annual data as of November 2022. Inflation is represented by the Consumer Price Index. Interest rates are represented by the Federal Funds rate.

As the above table shows, the first dollar peak took place in the 1980s as Fed chair Paul Volcker was aggressively hiking interest rates to fight inflation. As interest rates rose, investors flocked to the dollar, pushing it to record highs.

In the second strengthening cycle of the 1990s and 2000s emerging markets were growing at a considerable rate and buying U.S. dollar debt. During this time, a rising dollar hurt emerging market currencies and contributed to the Asian Financial Crisis of the 1990s. Here, currencies with high dollar-denominated debt but low U.S. dollar currency reserves struggled to pay off their debts.

During the Dotcom crash of 2002, the dollar hit its second peak.

The most recent cycle, since 2011, has been the longest strengthening cycle in decades. As the Federal Reserve moved to tighten monetary policy in the mid-2010s, the dollar’s strength accelerated. This has only been more pronounced in 2022 as the Fed hiked rates at the fastest rate in decades.

Weighing the Global Impact

As the below table shows, nearly all major global currencies have declined against the dollar:

| Currency | YTD Performance Against the U.S. Dollar* |

|---|---|

| Brazilian Real | 4.7% |

| Mexican Peso | 3.2% |

| Swiss Fanc | -2.5% |

| Australian Dollar | -6.9% |

| Canadian Dollar | -7.4% |

| Euro | -7.3% |

| Chinese Yuan | -8.9% |

| British Pound | -9.2% |

| Swedish Krona | -12.3% |

| Japanese Yen | -16.4% |

Source: Google Finance (Dec 2022). *Year-to-date performance as of Dec 12, 2022.

The main exceptions are the Brazilian real and Mexican peso. In anticipation of U.S. central bank rate hikes, both countries raised interest rates swiftly, creating higher yields for investors. In addition to being ahead of U.S. rate increases, both countries are energy producers.

By contrast, countries reliant on importing energy have seen weaker currencies. This includes the Japanese yen, Swedish krona, and the British pound. In the case of China, a weaker currency is the impact of a slow economic growth outlook due to its strict zero-COVID-19 strategy and low interest rates.

Europes grim economic prospects driven by the energy crisis have also pushed down the euro, with the currency reaching parity with the dollar in 2022 for the first time in two decades.

Bringing it All Together

Generally speaking, a strong dollar leads to weaker global growth. As U.S. imports get more expensive, it drives up inflation across countries.

When the U.S. dollar is strong it also makes U.S. assets pricier compared to foreign assets, which could impact the direction of capital flows. If the dollar remains strong, capital flows may be redirected away from America.

Finally, in the U.S., a strong dollar could weaken growth and lower inflation, serving as a mixed blessing for investors and consumers alike.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

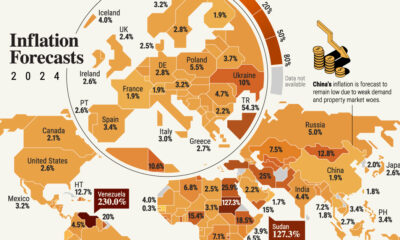

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

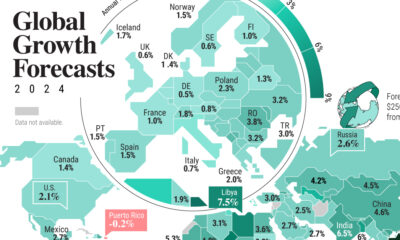

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022