Markets in a Minute

How Do Countries Around the World Compensate for Equity Risk?

This Markets in a Minute Chart is available as a poster.

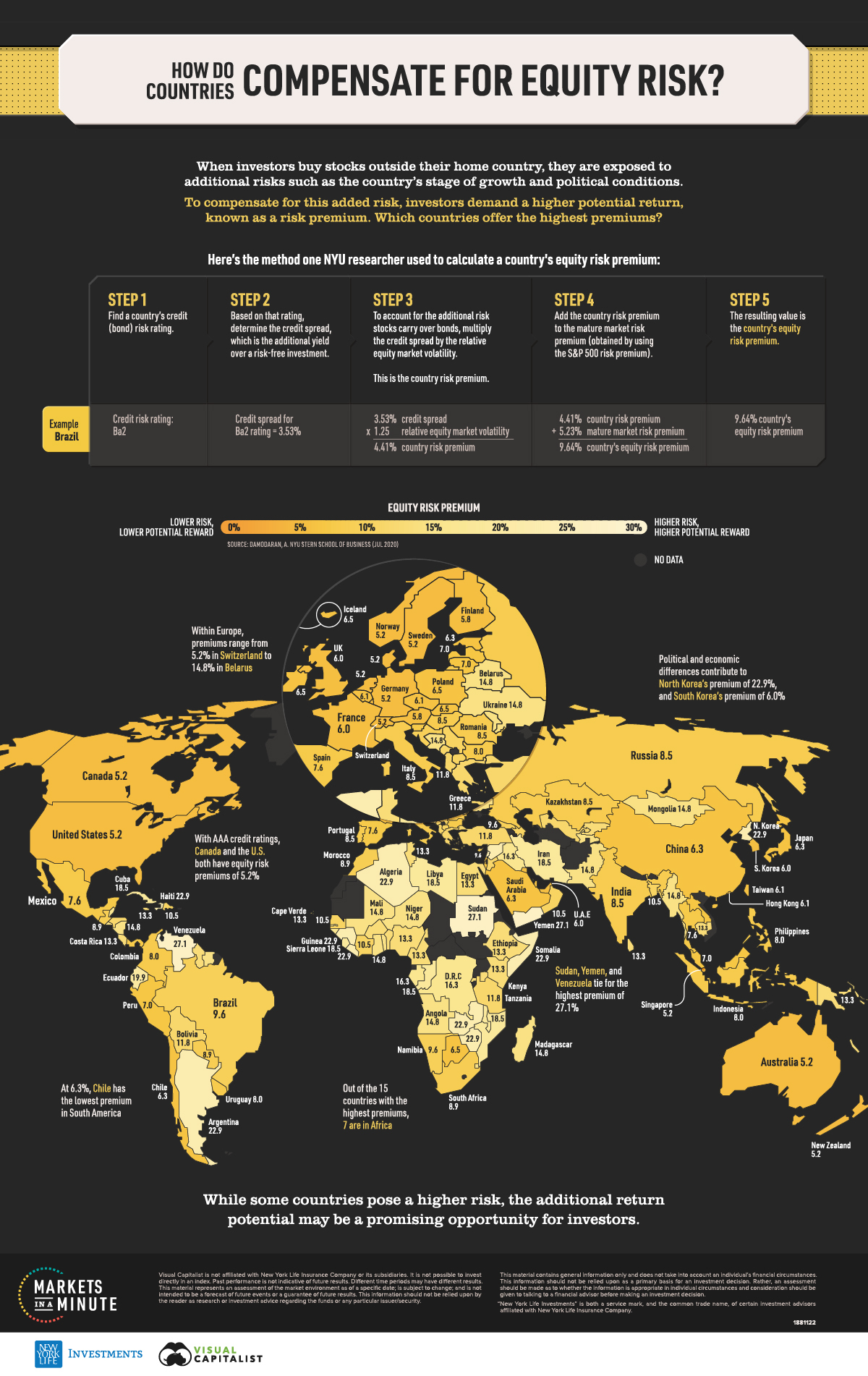

How Do Countries Compensate Investors for Equity Risk?

When investors purchase stocks internationally, they are exposed to additional risks. Companies may have higher volatility based on a country’s economic, political, and legal conditions. In exchange for taking on the additional risk, investors demand a higher return potential, known as an equity risk premium.

Which countries have the highest premiums? In this Markets in a Minute from New York Life Investments, we explore equity risk premiums for countries around the world.

Behind the Numbers

The premiums are based on a study by a New York University researcher, Aswath Damodaran. All data is as of July 1, 2020.

Here are the steps Damodaran took to determine a country’s equity risk premium:

| Step | Example - Brazil |

|---|---|

| 1. Find a country’s credit (bond) risk rating. | Credit risk rating: Ba2 |

| 2. Based on that rating, determine the credit spread, which is the additional yield over a risk-free investment. | Credit spread for Ba2 rating = 3.53% |

| 3. To account for the additional risk stocks carry over bonds, multiply the credit spread by the relative equity market volatility. This is the country risk premium. | 3.53% credit spread x 1.25 relative equity market volatility = 4.41% country risk premium |

| 4. Add the country risk premium to the mature market risk premium (obtained by using the S&P 500 risk premium). | 4.41% country risk premium + 5.23% mature market risk premium |

| 5. The resulting value is the country equity risk premium. | 9.64% country equity risk premium |

Premiums will shift over time as a country’s credit rating, credit spread, and equity market volatility changes.

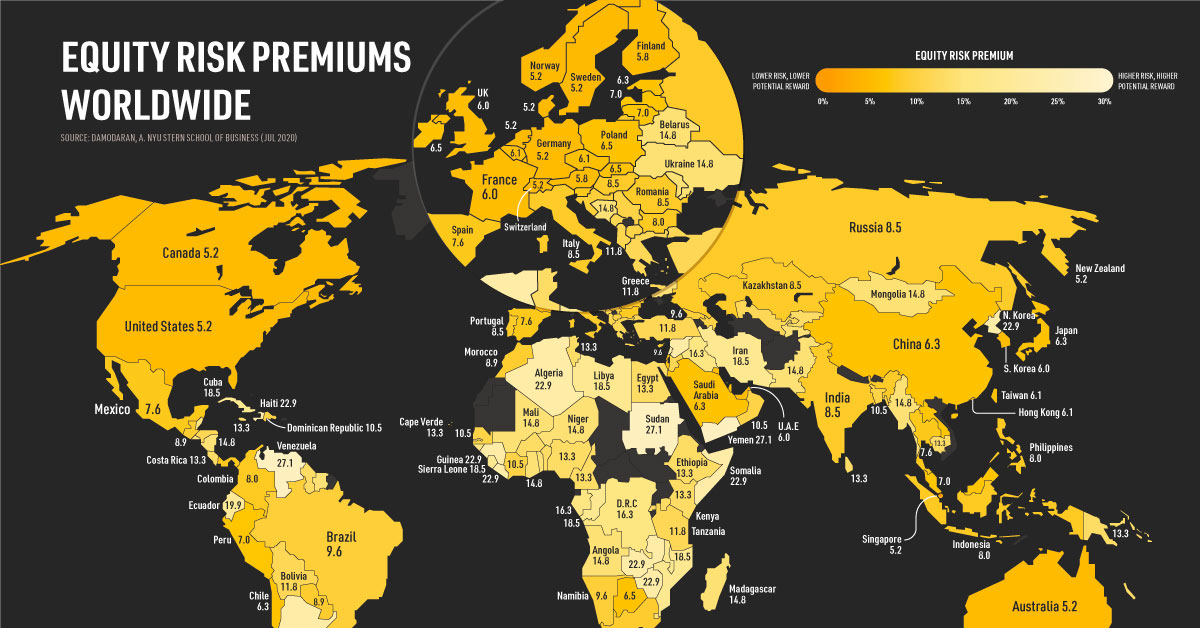

Equity Risk Premiums by Country

Below, we look at how equity risk premiums break down for 177 countries and regions, organized from highest to lowest.

| Country | Equity Risk Premium |

|---|---|

| Sudan | 27.14% |

| Venezuela | 27.14% |

| Yemen, Republic | 27.14% |

| Algeria | 22.86% |

| Argentina | 22.86% |

| Guinea | 22.86% |

| Haiti | 22.86% |

| Korea, D.P.R. | 22.86% |

| Lebanon | 22.86% |

| Liberia | 22.86% |

| Somalia | 22.86% |

| Syria | 22.86% |

| Zambia | 22.86% |

| Zimbabwe | 22.86% |

| Ecuador | 19.92% |

| Congo (Republic of) | 18.46% |

| Cuba | 18.46% |

| Iran | 18.46% |

| Libya | 18.46% |

| Malawi | 18.46% |

| Mozambique | 18.46% |

| Sierra Leone | 18.46% |

| Barbados | 16.25% |

| Belize | 16.25% |

| Congo (Democratic Republic of) | 16.25% |

| Gabon | 16.25% |

| Guinea-Bissau | 16.25% |

| Iraq | 16.25% |

| Angola | 14.79% |

| Belarus | 14.79% |

| Bosnia and Herzegovina | 14.79% |

| El Salvador | 14.79% |

| Gambia | 14.79% |

| Ghana | 14.79% |

| Madagascar | 14.79% |

| Maldives | 14.79% |

| Mali | 14.79% |

| Moldova | 14.79% |

| Mongolia | 14.79% |

| Myanmar | 14.79% |

| Nicaragua | 14.79% |

| Niger | 14.79% |

| Pakistan | 14.79% |

| Solomon Islands | 14.79% |

| St. Vincent & the Grenadines | 14.79% |

| Suriname | 14.79% |

| Tajikistan | 14.79% |

| Togo | 14.79% |

| Ukraine | 14.79% |

| Bahrain | 13.32% |

| Benin | 13.32% |

| Burkina Faso | 13.32% |

| Cambodia | 13.32% |

| Cameroon | 13.32% |

| Cape Verde | 13.32% |

| Costa Rica | 13.32% |

| Egypt | 13.32% |

| Ethiopia | 13.32% |

| Guyana | 13.32% |

| Jamaica | 13.32% |

| Kenya | 13.32% |

| Kyrgyzstan | 13.32% |

| Nigeria | 13.32% |

| Papua New Guinea | 13.32% |

| Rwanda | 13.32% |

| Sri Lanka | 13.32% |

| Swaziland | 13.32% |

| Tunisia | 13.32% |

| Uganda | 13.32% |

| Albania | 11.84% |

| Bolivia | 11.84% |

| Cook Islands | 11.84% |

| Greece | 11.84% |

| Honduras | 11.84% |

| Jordan | 11.84% |

| Montenegro | 11.84% |

| Tanzania | 11.84% |

| Turkey | 11.84% |

| Uzbekistan | 11.84% |

| Armenia | 10.52% |

| Bangladesh | 10.52% |

| Côte d'Ivoire | 10.52% |

| Dominican Republic | 10.52% |

| Fiji | 10.52% |

| Macedonia | 10.52% |

| Oman | 10.52% |

| Senegal | 10.52% |

| Serbia | 10.52% |

| Vietnam | 10.52% |

| Azerbaijan | 9.64% |

| Bahamas | 9.64% |

| Brazil | 9.64% |

| Croatia | 9.64% |

| Cyprus | 9.64% |

| Georgia | 9.64% |

| Namibia | 9.64% |

| Guatemala | 8.90% |

| Morocco | 8.90% |

| Paraguay | 8.90% |

| South Africa | 8.90% |

| Trinidad and Tobago | 8.90% |

| Hungary | 8.46% |

| India | 8.46% |

| Italy | 8.46% |

| Kazakhstan | 8.46% |

| Montserrat | 8.46% |

| Portugal | 8.46% |

| Romania | 8.46% |

| Russia | 8.46% |

| St. Maarten | 8.46% |

| Andorra (Principality of) | 8.03% |

| Bulgaria | 8.03% |

| Colombia | 8.03% |

| Curacao | 8.03% |

| Indonesia | 8.03% |

| Philippines | 8.03% |

| Sharjah | 8.03% |

| Uruguay | 8.03% |

| Aruba | 7.58% |

| Mauritius | 7.58% |

| Mexico | 7.58% |

| Panama | 7.58% |

| Slovenia | 7.58% |

| Spain | 7.58% |

| Thailand | 7.58% |

| Turks and Caicos Islands | 7.58% |

| Laos | 6.99% |

| Latvia | 6.99% |

| Lithuania | 6.99% |

| Malaysia | 6.99% |

| Peru | 6.99% |

| Bermuda | 6.48% |

| Botswana | 6.48% |

| Brunei | 6.48% |

| Iceland | 6.48% |

| Ireland | 6.48% |

| Malta | 6.48% |

| Poland | 6.48% |

| Ras Al Khaimah (Emirate of) | 6.48% |

| Slovakia | 6.48% |

| Chile | 6.26% |

| China | 6.26% |

| Estonia | 6.26% |

| Israel | 6.26% |

| Japan | 6.26% |

| Saudi Arabia | 6.26% |

| Belgium | 6.12% |

| Cayman Islands | 6.12% |

| Czech Republic | 6.12% |

| Guernsey (States of) | 6.12% |

| Hong Kong | 6.12% |

| Jersey (States of) | 6.12% |

| Macao | 6.12% |

| Qatar | 6.12% |

| Taiwan | 6.12% |

| Abu Dhabi | 5.96% |

| France | 5.96% |

| Isle of Man | 5.96% |

| Korea | 5.96% |

| Kuwait | 5.96% |

| United Arab Emirates | 5.96% |

| United Kingdom | 5.96% |

| Austria | 5.81% |

| Finland | 5.81% |

| Australia | 5.23% |

| Canada | 5.23% |

| Denmark | 5.23% |

| Germany | 5.23% |

| Liechtenstein | 5.23% |

| Luxembourg | 5.23% |

| Netherlands | 5.23% |

| New Zealand | 5.23% |

| Norway | 5.23% |

| Singapore | 5.23% |

| Sweden | 5.23% |

| Switzerland | 5.23% |

| United States | 5.23% |

Venezuela, Sudan, and Yemen are tied for the highest equity risk premium. While Venezuela battles hyperinflation, Yemen is suffering from a humanitarian crisis and Sudan has high perceived corruption.

In the mid-range, emerging countries such as Brazil, South Africa, and India carry moderate risk. However, they may also provide investors with higher returns than can be expected in mature markets.

On the low end of the scale, countries such as the United States, Singapore, and Germany have AAA credit ratings and the lowest premium of 5.23%.

Applying Risk Premiums to Companies

How can investors determine the equity risk premiums for individual companies?

One method is to assume that all companies incorporated in a country have equal exposure to that country’s risk. However, this is a simplified approach and does not account for the fact that a company’s operations may extend into other markets.

Alternatively, investors can calculate a weighted-average premium based on the location of a company’s revenue or production. For example, a consumer products business may weigh exposure based on the location of their revenue. An oil and gas company, where true risk lies in their reserves rather than where they sell, may instead be weighted by production.

Here’s a hypothetical example for an oil & gas company that has reserves in the United States, Saudi Arabia, and Venezuela:

| Country | Production (in kboed)* | % of Total | Equity Risk Premium |

|---|---|---|---|

| U.S. | 60 | 20% | 5.23% |

| Saudi Arabia | 120 | 40% | 6.26% |

| Venezuela | 120 | 40% | 27.14% |

| Total | 300 | 100% | 14.41% |

* Kilobarrels of oil equivalent per day.

The weighted-average equity risk premium is 14.41%.

Importantly, even countries headquartered in mature markets have international risks if they carry out operations in other countries.

Risk Vs. Potential Reward

Every country presents varying degrees of risk based on local conditions. As investors look to diversify internationally, it’s critical to consider two factors:

- The additional risk

- The potential additional return

Equity risk premiums serve as a guide that can help investors compare country risk, and the additional return potential they should expect for tolerating that risk.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022