Markets in a Minute

Which ESG Risks Are Affecting Your Portfolio?

This Markets in a Minute Chart is available as a poster.

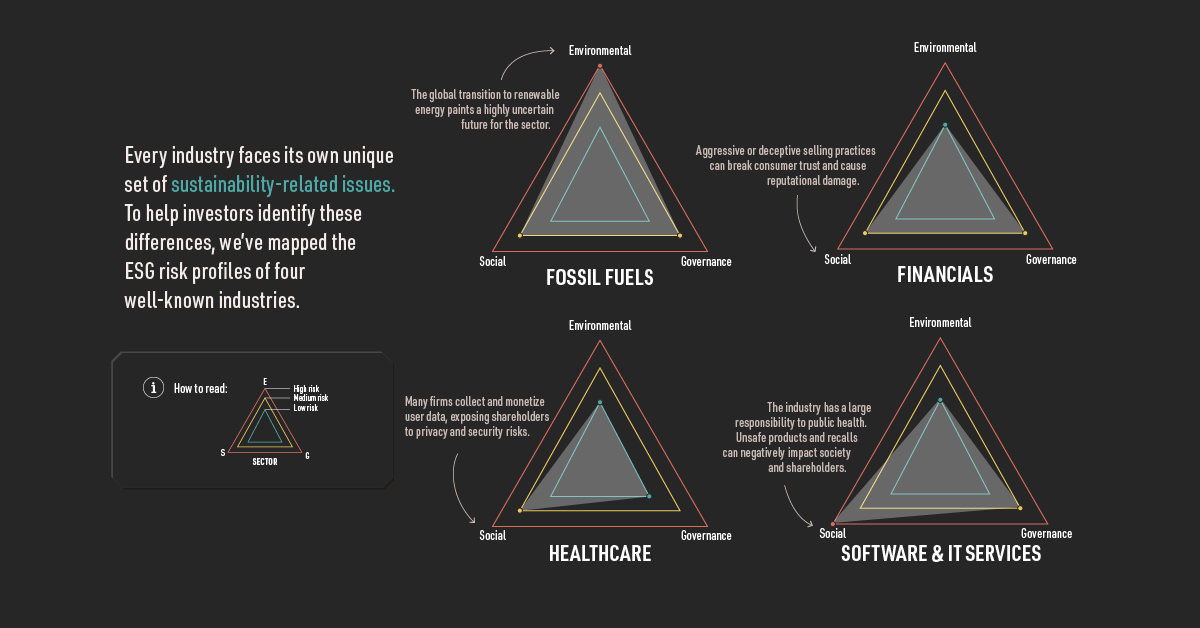

Visualizing ESG Risk by Industry

Aging populations, climate change, and data security are some of the world’s most pressing issues, but what theme do they all share? For investors, the answer is certain: sustainability.

Sustainability is a concept that’s quickly moved into the mainstream, and is best described as the consideration of environmental, social, and governance (ESG) factors when analyzing companies. Combining these non-financial metrics with traditional analysis has been proven to have a positive influence on long-term returns.

In this Markets in a Minute chart from New York Life Investments, we’ve mapped the ESG risk profiles of four prominent industries to gain a better understanding of the sustainability issues they’re likely facing.

Fossil Fuels

Investors in this sector have substantial exposure to all three ESG risks, with environmental issues being the most significant.

| Risk | Importance | Issues to Consider |

|---|---|---|

Environmental | High |

|

Social | Medium |

|

Governance | Medium |

|

The global transition to renewable energy paints a complex future for the sector, though it’s uncertain when oil demand will peak—predictions range from 2025 all the way to 2040. Nevertheless, market participants are taking action. To date, over 1,200 institutional investors representing $14 trillion in assets have made commitments to divest from fossil fuels.

Social risks are another source of uncertainty, especially as public awareness around climate change increases. A planned expansion of the Keystone Pipeline System, referred to as Keystone XL, has faced nearly a decade of public resistance and currently remains blocked by the U.S. Supreme Court.

Last but not least are governance risks. With many investors considering the switch to a fossil fuel-free portfolio, shareholder transparency will be of utmost importance. The onus will be on company management to demonstrate that they have a clear understanding of the risks and opportunities ahead. Royal Dutch Shell, the world’s fourth largest oil company, has made progress on this front by announcing its strategy for achieving net-zero emissions by 2050.

Financials

Social and governance risks are the top priorities for investors in the financial sector. Firms that finance the fossil fuel industry may have indirect exposure to environmental risks.

| Risk | Importance | Issues to Consider |

|---|---|---|

Environmental | Low |

|

Social | Medium |

|

Governance | Medium |

|

Underpinning the strength of the financial sector is consumer trust and client service. By using aggressive or deceptive selling practices, firms risk severe reputational damage and even financial penalties. Wells Fargo, America’s fourth largest bank, was recently fined $3 billion for its account fraud scandal that emerged in 2016.

These issues are closely related to governance risks, where weak internal structures can allow fraudulent activities like money laundering to take place. In fact, over a 15 month period ending in 2019, global banks were fined $10 billion for engaging in the activity. Experts believe that 60% of laundering fines resulted from criminals slipping past screening systems.

Healthcare

Social risks are the top concern for healthcare investors, given the sector’s important role in public health and well-being.

| Risk | Importance | Issues to Consider |

|---|---|---|

Environmental | Low |

|

Social | Medium |

|

Governance | Low |

|

Unsafe products are one the most clear-cut issues because they directly harm society and shareholders. Johnson & Johnson, one of the world’s largest healthcare companies, has faced thousands of lawsuits for failing to warn consumers about asbestos in its baby powder products. The company was recently ordered to pay $2.1 billion in damages by a Missouri appeals court.

The use of inappropriate advertising is another issue that investors may want to watch out for. In 2019, Mundipharma was fined by the Australian government for making inaccurate statements in its marketing materials for opioids.

Software & IT Services

Companies in this sector are exposed to various social and governance risks, but are not known to be large polluters.

| Risk | Importance | Issues to Consider |

|---|---|---|

Environmental | Low |

|

Social | High |

|

Governance | Medium |

|

Many firms in this industry collect and monetize user data, exposing their shareholders to data privacy and security risks. Facebook has been at the center of numerous controversies in recent years, including the Cambridge Analytica scandal, which saw the unconsented collection of personal data from 87 million users. Polls found that 44% of Facebook users viewed the platform more negatively after the scandal.

These risks are likely to be amplified as governments take a firmer stance on data regulation. In 2018, the EU implemented its General Data Protection Regulation (GDPR), one of the world’s toughest privacy and security laws. In certain cases, noncompliance with the GDPR can result in fines equal to 4% of a company’s global revenues.

Navigating an Uncertain Future

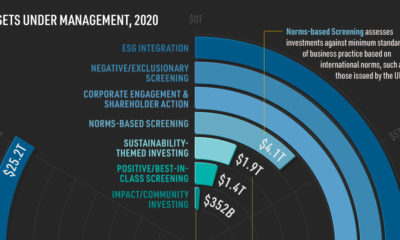

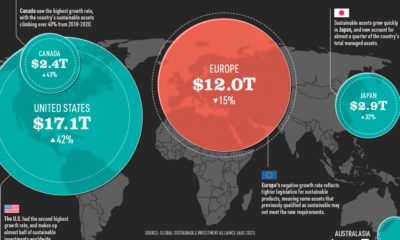

Global sustainability issues are creating a more challenging environment for businesses in all types of industries. To hedge these risks, investors are turning to ESG in massive numbers—the value of sustainably managed assets now sits at $40.5 trillion, nearly double the amount from four years ago.

It’s important to remember, however, that businesses are unique. A social issue affecting one industry may not be as relevant for another. When armed with this knowledge, investors will be able to make more informed decisions that strengthen the long-term resiliency of their portfolios.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators