Markets in a Minute

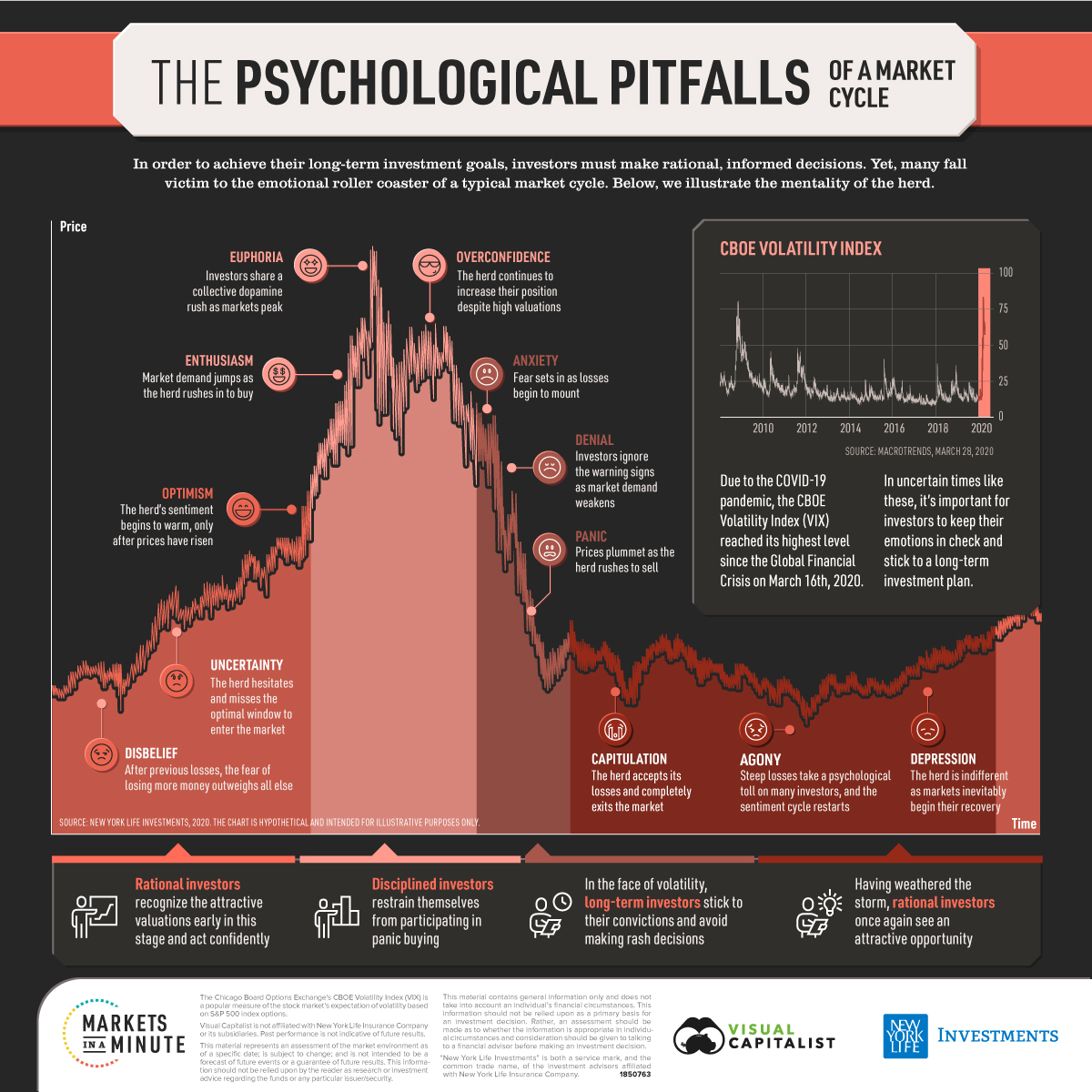

The Psychological Pitfalls of a Market Cycle

This Markets in a Minute Chart is available as a poster.

This Markets in a Minute Chart is available as a poster.

The Psychological Pitfalls of a Market Cycle

When making investment decisions, investors have a wide variety of tools at their disposal.

For example, fundamental analysis can be used to estimate a stock’s intrinsic value. Technical analysis, on the other hand, requires an investor to analyze price movements to identify trends.

While these tools can form the basis of a sound investment thesis, their effectiveness is limited by one’s emotions. In today’s Markets in a Minute chart from New York Life Investments, we illustrate how sentiment can get in the way of rational decision making.

The Mentality of the Herd

Allowing emotions to dictate decisions is a common mistake made by many investors, yet they may not even realize it.

Herd mentality, which refers to an individual’s tendency to be influenced by his or her peers, often leads to heightened emotions and less rational decision making. In the context of investing, this tendency becomes particularly troublesome—market developments can be sensationalized in the media, by online blogs, or through word-of-mouth.

Mapping the Sentiment Cycle

Similar to how markets move in a series of patterns and cycles, the behavior of the investor herd tends to follow a continuous “sentiment cycle.”

1. Market Recovery

Today’s chart begins at the recovery stage of a market cycle, and assumes that emotional investors have recently suffered losses.

Although a support level has been clearly established, the herd is likely too afraid to act. Their fear of making another mistake causes them to miss the optimal window to re-enter the market.

2. Market Peak

Only after prices have substantially risen does the herd begin to take notice. Many of these investors will experience the fear of missing out (FOMO), and overzealously begin buying. Valuations at this point are likely no longer attractive.

3. Market Decline

What comes up must come down, and prices eventually peak as demand weakens. Investors who become too emotionally attached can find it difficult to cut their losses early.

4. Market Trough

By this point, the sentiment cycle has run a full course. Investors who followed the herd have likely sold at a loss, and will be reluctant to re-enter the market again.

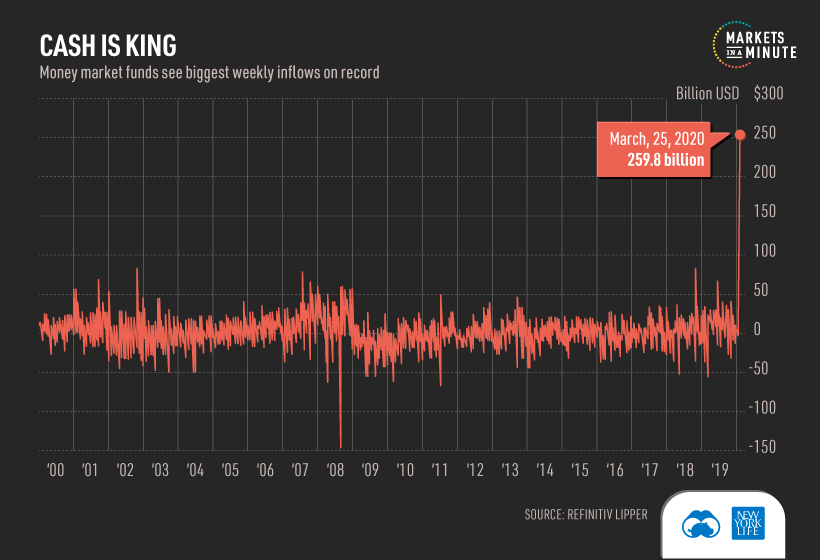

Navigating Rough Waters

Investors are prone to falling into the sentiment cycle at any time, but especially when things get rough. So-called black swan events, such as the COVID-19 pandemic, can bring volatility to markets on short notice. In these situations, it’s common for investors to flock to safe-haven assets.

Since COVID-19 was classified as a global pandemic, money market funds have been in extremely high demand:

While this dramatic shift does have its merits—equity markets have seen deep selloffs—it may be a tad drastic. Governments around the world are making serious commitments to providing economic stimulus. In the U.S., the CARES Act amounts to a massive $2 trillion, and provides direct payments to families as well as support for both the private and public sector.

Keeping a Clear Mind

Now that we’ve outlined the psychological pitfalls of a market cycle, what can one do to break away from the herd?

A good start is becoming aware of the cognitive biases we commonly exhibit when investing. These biases can be linked to many of the emotions outlined in today’s chart. Finally, maintaining a growth mindset and learning from our past mistakes can also help us make better decisions in the future.

Markets in a Minute

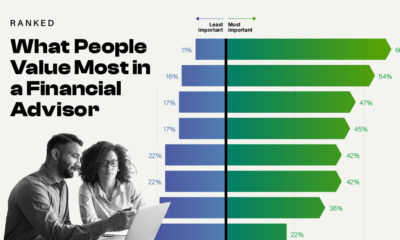

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022