Markets in a Minute

Dividend Stocks: Driving Value in Volatile Markets

This Markets in a Minute Chart is available as a poster.

This Markets in a Minute Chart is available as a poster.

Dividend Stocks: Driving Value in Volatile Markets

When markets take a turn for the worse, dividends often can provide a buffer against the drop.

Year after year, dividend-paying companies put money into shareholders’ pockets—and may offer much needed stability during periods of high volatility. Dividend investing can help offset unexpected downturns by generating a key source of income.

In today’s Markets in a Minute chart from New York Life Investments, we explore how dividends can help lower risk within investors portfolios when markets enter turbulent territory.

The Appeal of Dividends

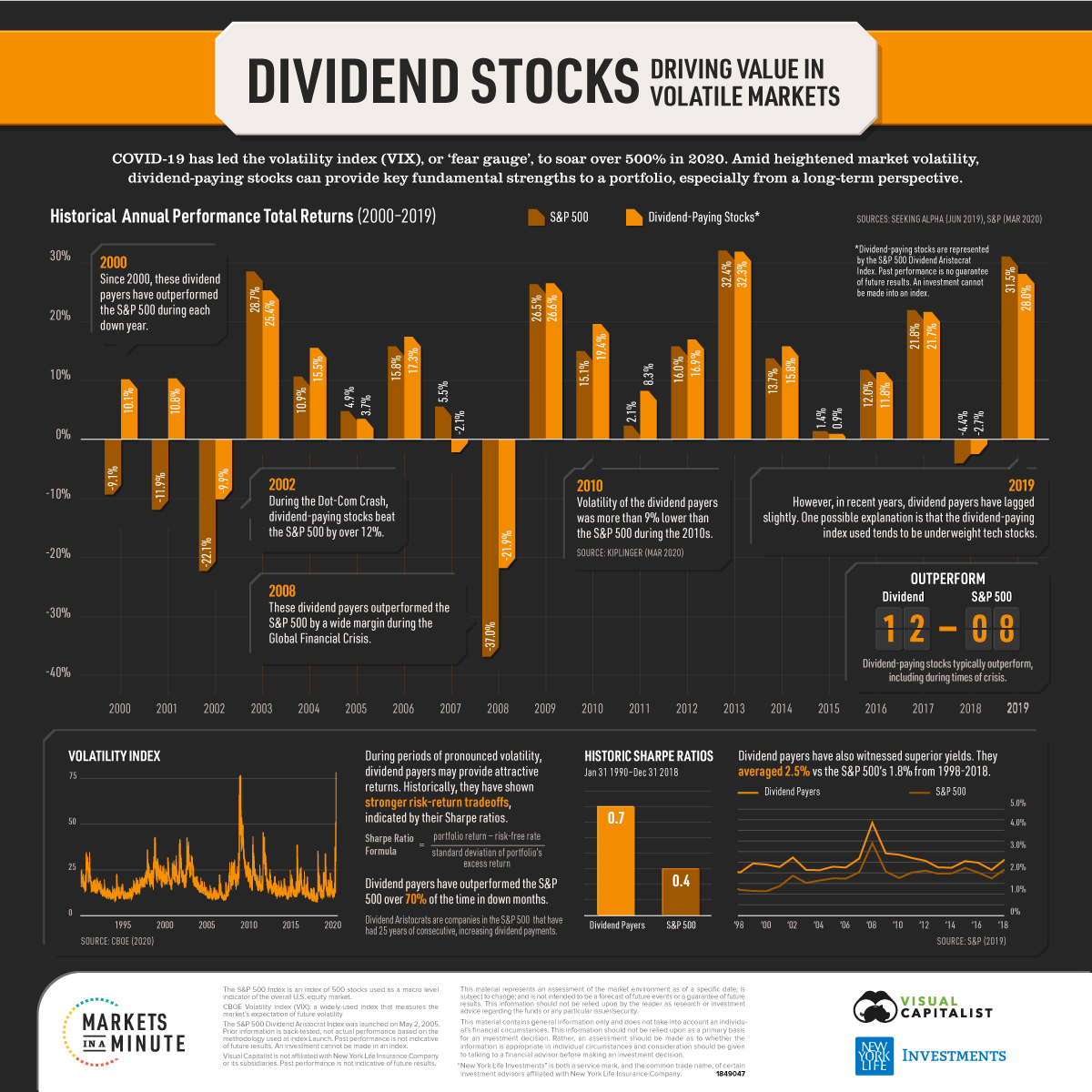

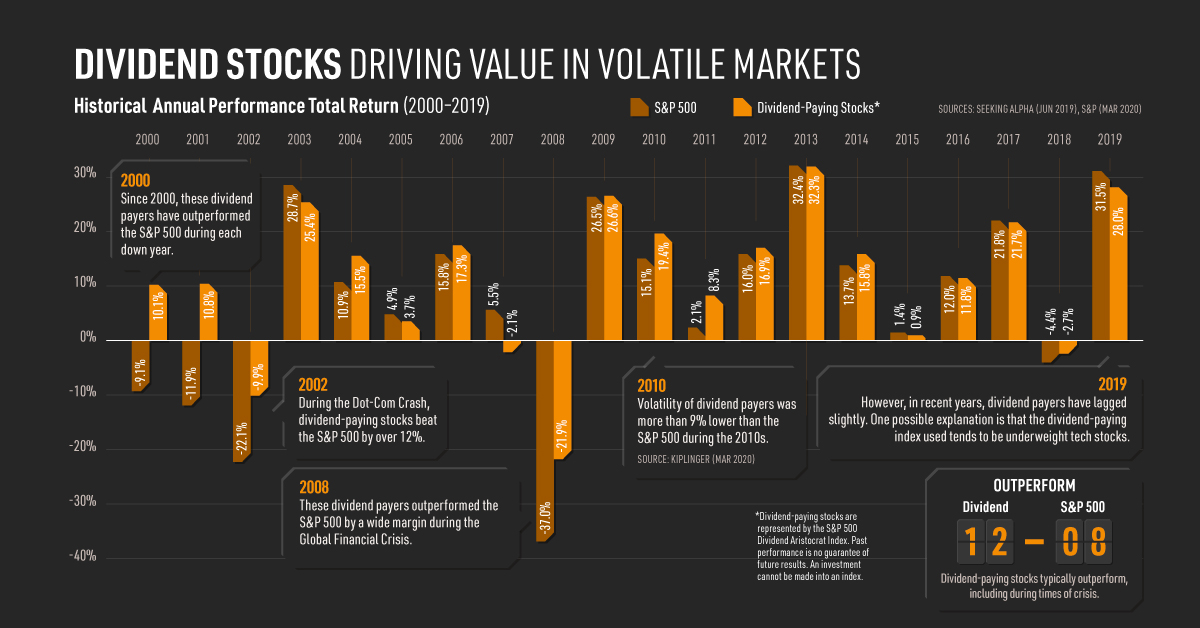

Over the last two decades, dividend-paying companies have outperformed the S&P 500 in 12 of 20 years, including in all five years where the S&P 500 finished the year in negative territory.

| Year | S&P 500 Total Return (TR) | Dividend-Paying Stocks* Total Return (TR) | Top performer |

|---|---|---|---|

| 2000 | -9.1% | 10.1% | Dividends |

| 2001 | -11.9% | 10.8% | Dividends |

| 2002 | -22.1% | -9.9% | Dividends |

| 2003 | 28.7% | 25.4% | S&P 500 |

| 2004 | 10.9% | 15.5% | Dividends |

| 2005 | 4.9% | 3.7% | S&P 500 |

| 2006 | 15.8% | 17.3% | Dividends |

| 2007 | 5.5% | -2.1% | S&P 500 |

| 2008 | -37.0% | -21.9% | Dividends |

| 2009 | 26.5% | 26.6% | Dividends |

| 2010 | 15.1% | 19.4% | Dividends |

| 2011 | 2.1% | 8.3% | Dividends |

| 2012 | 16.0% | 16.9% | Dividends |

| 2013 | 32.4% | 32.3% | S&P 500 |

| 2014 | 13.7% | 15.8% | Dividends |

| 2015 | 1.4% | 0.9% | S&P 500 |

| 2016 | 12.0% | 11.8% | S&P 500 |

| 2017 | 21.8% | 21.7% | S&P 500 |

| 2018 | -4.4% | -2.7% | Dividends |

| 2019 | 31.5% | 28.0% | S&P 500 |

*Dividend stocks represented by S&P 500 Dividend Aristocrat Index. Past performance is no guarantee of future results.

What sets dividend-paying companies—and especially those that continually grow their dividends—apart from the herd?

Wide Moats: A Competitive Advantage

While dividend growth signals company strength, it can also indicate that the company has an economic moat—a sustainable competitive advantage. This means two things: the company can raise prices, and keep competitors at bay. For shareholders, this signals a stronger likelihood of profitability, and more sustainable dividend payouts.

Reinvested Income Fuel Returns

Between 1926 and 2018, reinvested dividend income accounted for 33% of total equity returns in the S&P 500.

While capital appreciation is an undisputed factor in building wealth, it’s easy to forget the sheer force of dividends.

Strong Balance Sheet

A company’s ability to pay steady dividends is critical. Dividends are drawn from a company’s cash balance, which must be sufficient during both strong and lackluster financial conditions.

Ultimately, this cash allocation represents a conservative and disciplined approach to the company balance sheet—demonstrating a commitment to shareholders.

“At the end of the day, dividends are not being paid with margins; dividends are paid with earnings per share.”

—Joe Kaeser

Cushion Against a Shock

When markets turn sour, income from dividend payouts can offer a key lifeline.

The ability for dividend payers to generate superior risk-adjusted returns is demonstrated across their Sharpe ratios, with a higher number indicating a more attractive risk/return profile.

For instance, between 1990-2018, The S&P 500 Dividend Aristocrat Index—a basket of stocks that have paid consistent, increasing, dividends over 25 years— averaged a Sharpe ratio of 0.7 compared to the S&P 500’s 0.4.

Alongside this, a number of dividend payers have outperformed the S&P 500 in every down year since 2000.

| Year | S&P 500 Total Return (TR) | Dividend-Paying Stocks* Total Return (TR) |

|---|---|---|

| 2000 | -9.1% | 10.1% |

| 2001 | -11.9% | 10.8% |

| 2002 | -22.1% | -9.9% |

| 2008 | -37% | -21.9% |

| 2018 | -4.4% | -2.7% |

| Total Years Dividend-Paying Stocks (TR) Outperformed | 5 |

*Dividend stocks represented by S&P 500 Dividend Aristocrat Index. Past performance is no guarantee of future results.

Even during dismal years, dividend payers have shown notable returns.

A Powerful Tool in Today’s Market

As COVID-19 continues to drive further volatility in the market, dividend investing may offer investors both stability and strong income to help weather the storm.

Of course, not all dividend-payers can be expected to be winners. Careful analysis of financial statements and management track records is required to identify companies with the strongest fundamentals.

While dividend payers can help provide a shield in volatile markets, they double as a significant driver of wealth creation over time.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators