Markets in a Minute

The Potential Cost of Trying to Time the Stock Market

The Potential Cost of Trying to Time the Stock Market

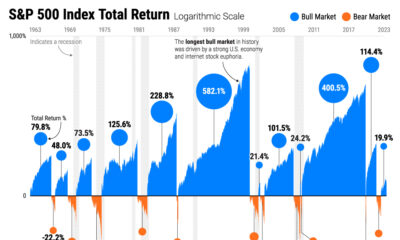

Timing the market seems simple enough: buy when prices are low and sell when they’re high.

But there is clear evidence that market timing is difficult. Often, investors will sell early, missing out on a stock market rally. It can also be unnerving to invest when the market is flashing red.

By contrast, staying invested through highs and lows has generated competitive returns, especially over longer periods.

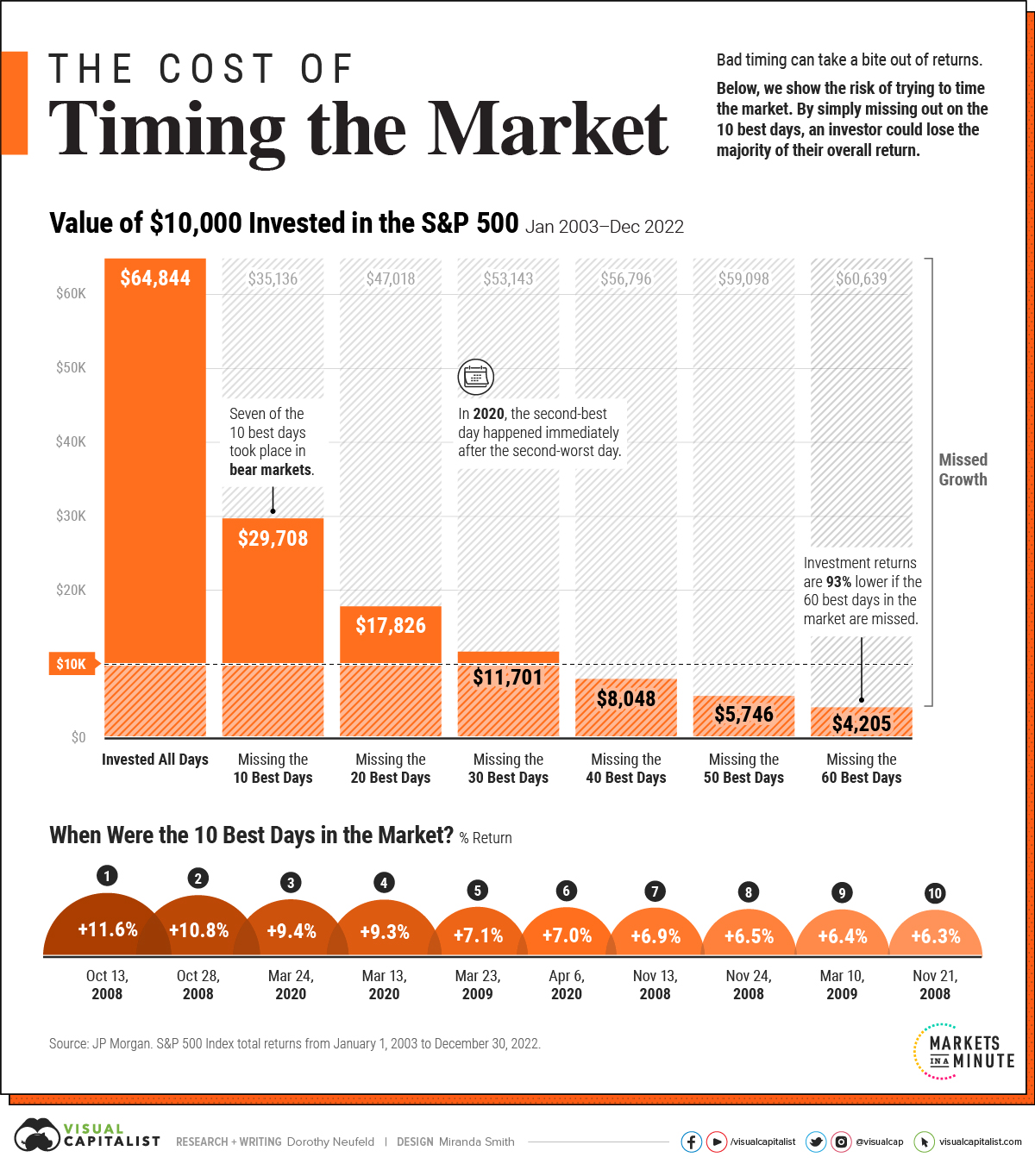

The above graphic shows how trying to time the market can take a bite out of your portfolio value, using 20 years of data from JP Morgan.

The Pitfalls of Timing the Market

Mistiming the market even by just a few days can significantly affect an investor’s returns.

The following scenarios compare the total returns of a $10,000 investment in the S&P 500 between January 1, 2003 and December 30, 2022. Specifically, it highlights the impact of missing the best days in the market compared to sticking to a long-term investment plan.

| $10,000 Invested in the S&P 500 End Portfolio Value | Annual Return (2003-2022) | |

|---|---|---|

| Invested All Days | $64,844 | +9.8% |

| Missed 10 Best Days | $29,708 | +5.6% |

| Missed 20 Best Days | $17,826 | +2.9% |

| Missed 30 Best Days | $11,701 | +0.8% |

| Missed 40 Best Days | $8,048 | -1.1% |

| Missed 50 Best Days | $5,746 | -2.7% |

| Missed 60 Best Days | $4,205 | -4.2% |

As we can see in the above table, the original investment grew over sixfold if an investor was fully invested for all days.

If an investor were to simply miss the 10 best days in the market, they would have shed over 50% of their end portfolio value. The investor would finish with a portfolio of only $29,708, compared to $64,844 if they had just stayed put.

Making matters worse, by missing 60 of the best days, they would have lost a striking 93% in value compared to what the portfolio would be worth if they had simply stayed invested.

Overall, an investor would have seen almost 10% in average annual returns using a buy-and-hold strategy. Average annual returns entered negative territory once they missed the 40 best days over the time frame.

The Best Days in the Market

Why is timing the market so hard? Often, the best days take place during bear markets.

| Rank | Date | Return |

|---|---|---|

| 1 | Oct 13, 2008 | +12% |

| 2 | Oct 28, 2008 | +11% |

| 3 | Mar 24, 2020 | +9% |

| 4 | Mar 13, 2020 | +9% |

| 5 | Mar 23, 2009 | +7% |

| 6 | Apr 6, 2020 | +7% |

| 7 | Nov 13, 2008 | +7% |

| 8 | Nov 24, 2008 | +7% |

| 9 | Mar 10, 2009 | +6% |

| 10 | Nov 21, 2008 | +6% |

Over the last 20 years, seven of the 10 best days happened when the market was in bear market territory.

Adding to this, many of the best days take place shortly after the worst days. In 2020, the second-best day fell right after the second-worst day that year. Similarly, in 2015, the best day of the year occurred two days after its worst day.

Interestingly, the worst days in the market typically occurred in bull markets.

Why Staying Invested Benefits Investors

As historical data shows, the best days happen during market turmoil and periods of heightened market volatility. In missing the best days in the market, an investor risks losing out on meaningful return appreciation over the long run.

Not only does timing the market take considerable skill, it involves temperament, and a consistent track record. If there were bullet-proof signals for timing the market, they would be used by everyone.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022