Markets in a Minute

Visualizing 50 Years of Global Stock Markets (1970-Today)

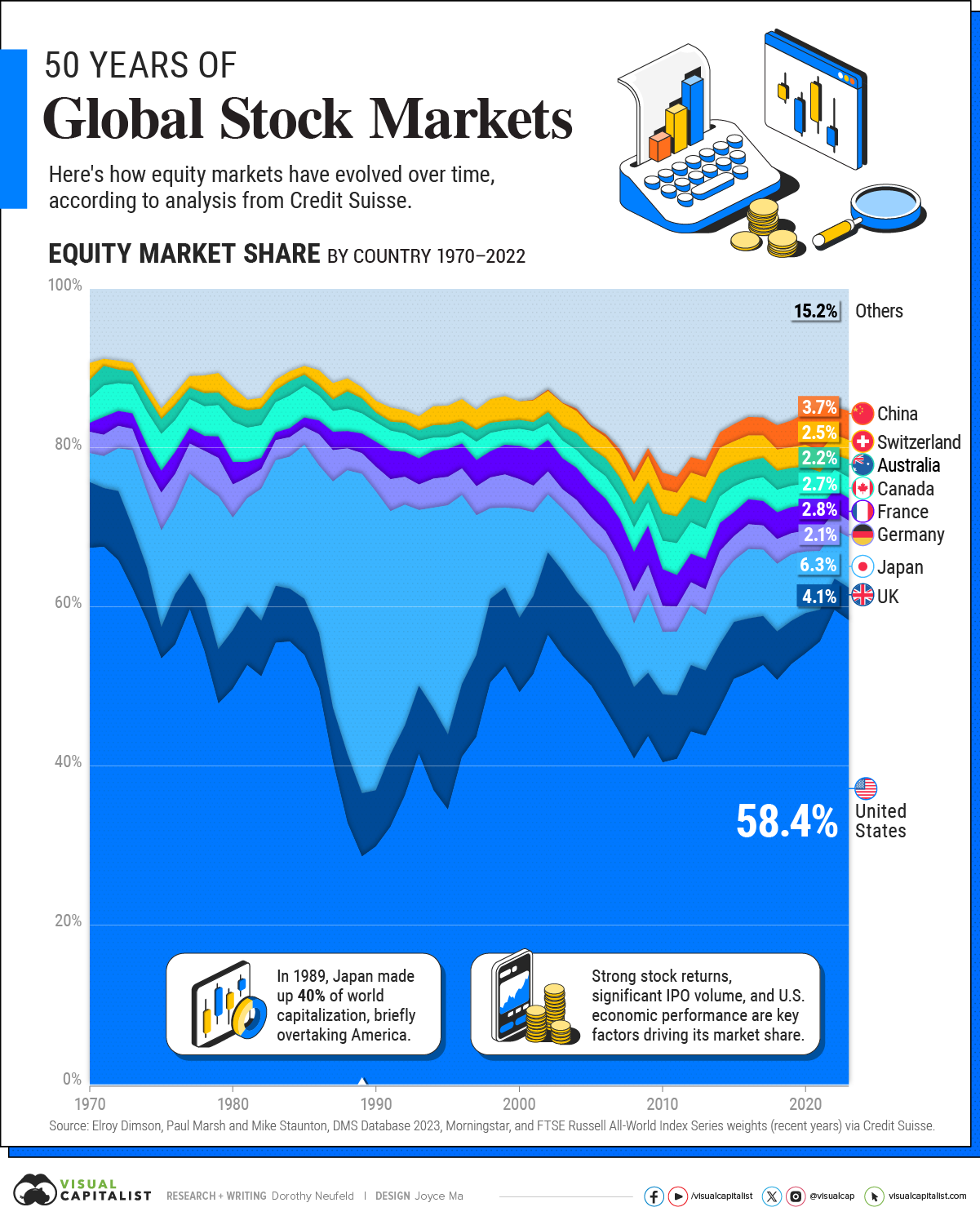

Visualizing 50 Years of Global Stock Markets

For decades, the U.S. has firmly remained the world’s financial power.

But how long will this continue, and what factors could underscore a new shift? To look at the role of the U.S. in the broader financial system, this graphic shows 50 years of global stock markets, with data from Credit Suisse.

Global Stock Markets Today

Today, the U.S. covers 58.4% of global equity markets as of year-end 2022.

| Top Stock Markets | Share of Global Stock Market 2022 |

|---|---|

| 🇺🇸 U.S. | 58.4% |

| 🇯🇵 Japan | 6.3% |

| 🇬🇧 U.K. | 4.1% |

| 🇨🇳 China | 3.7% |

| 🇫🇷 France | 2.8% |

| 🇨🇦 Canada | 2.7% |

| 🇨🇭 Switzerland | 2.5% |

| 🇦🇺 Australia | 2.2% |

| 🇩🇪 Germany | 2.1% |

| 🌎 Others | 15.2% |

The next largest stock market is Japan, at 6.3% of the global market share.

For a brief period in 1989, it overtook the U.S. when the Nikkei hit an all-time high following supercharged economic growth. However, after its subsequent crash and “lost decades”, it would take 33 years for Japan’s stock market to recover to those same highs.

Lastly, despite China being the world’s second-largest economy, it only accounts for just 3.7% of the world’s equity market share, a similar level as the UK.

Rise and Fall

Stock markets have been around for centuries.

While the New York Stock Exchange originated in 1792, Amsterdam’s stock market, arguably the world’s oldest, dates back to 1602.

During the mid-1700s, London began to overtake Amsterdam as a leading financial market amid growing financial activity and trade. An increasing number of firms set up offices in the city, bringing with them key business relationships.

After roughly 200 years, London’s role as a global financial center was surpassed by New York after WWII, driven by the economic crisis caused by the war.

America’s rise in prominence was supported by the growing credibility of the Federal Reserve, while the global status of the Bank of England diminished as the value of the pound weakened.

Given the destabilizing effects of the war, the U.S. filled the vacuum, emerging as a leading stock market supported by a robust economy and central bank—a position it continues to hold.

What Comes Next?

Why is America’s influence over global stock markets unrivaled?

The dollar’s status as a reserve currency plays a central role, along with the depth of its financial markets. Its economic, political, and military strength are other important factors.

America’s stock market returns have also outperformed nearly all other countries since 1900, attracting investors both domestically and abroad.

While American “declinism” has become a cliche, countries have risen and fallen over history. In the early 19th century, Britain’s publicly held debt soared from 109% of GDP in 1918 to roughly 200% by 1934. By around this time, its economic output had been exceeded by America, Germany, and the Soviet Union.

While there are key differences between the U.S. and Britain at that time, history suggests that balances in military power, debt, and economic dominance were key variables in the rise and decline of financial powers.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022