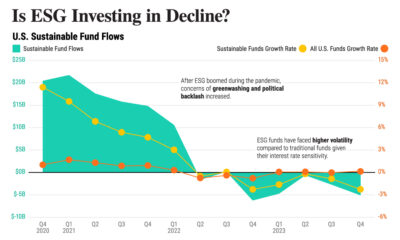

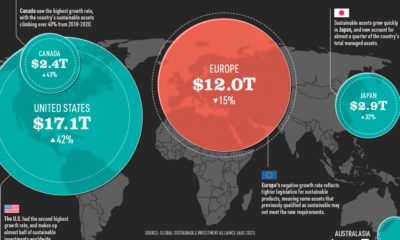

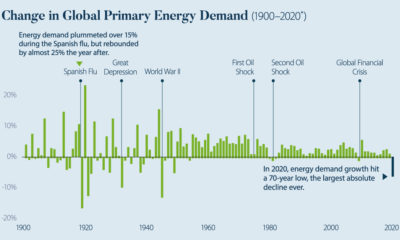

Markets in a Minute

Sustainable Investing Strategies by Popularity

This infographic is available as a poster.

This infographic is available as a poster.

Sustainable Investing Strategies by Popularity

If you wanted to invest sustainably in the 1960s, your options were fairly limited. Sustainable investing strategies kicked off with socially responsible investing, where investors could exclude stocks or entire industries from their portfolio based on business activities. For example, if you didn’t agree with smoking you could exclude tobacco production companies.

Fast forward 60 years, and investors have many more approaches available to them. From exclusionary screening to ESG integration, which strategy is the most popular? This Markets in a Minute from New York Life Investments shows global assets under management for various sustainable investing strategies, to see which ones are used the most and the least globally.

The Types of Sustainable Investing Strategies

Before we dive into the numbers, it’s helpful to know the definitions of the various sustainable investing strategies. The Global Sustainable Investment Alliance, who put together this data, has classified sustainable investing into the seven core strategies below.

- ESG integration: The explicit inclusion of environmental, social, and governance (ESG) factors into financial analysis

- Negative/exclusionary screening: The exclusion of certain sectors, companies, or countries based on activities considered not investable

- Corporate engagement & shareholder action: Influencing corporate behavior through actions such as shareholder proposals

- Norms-based screening: Screening investments based on international norms, such as those issued by the UN

- Sustainability-themed/thematic investing: Investing in themes specifically contributing to sustainable solutions, such as diversity

- Positive screening/best-in-class: Investment in sectors, companies, or projects with positive ESG performance relative to industry peers

- Impact/community investing: Investing to achieve positive ESG impacts, and/or investing in traditionally underserved communities

While these sustainable investing strategies differ in their approaches, they all require investors to consider ESG factors as they build and manage portfolios.

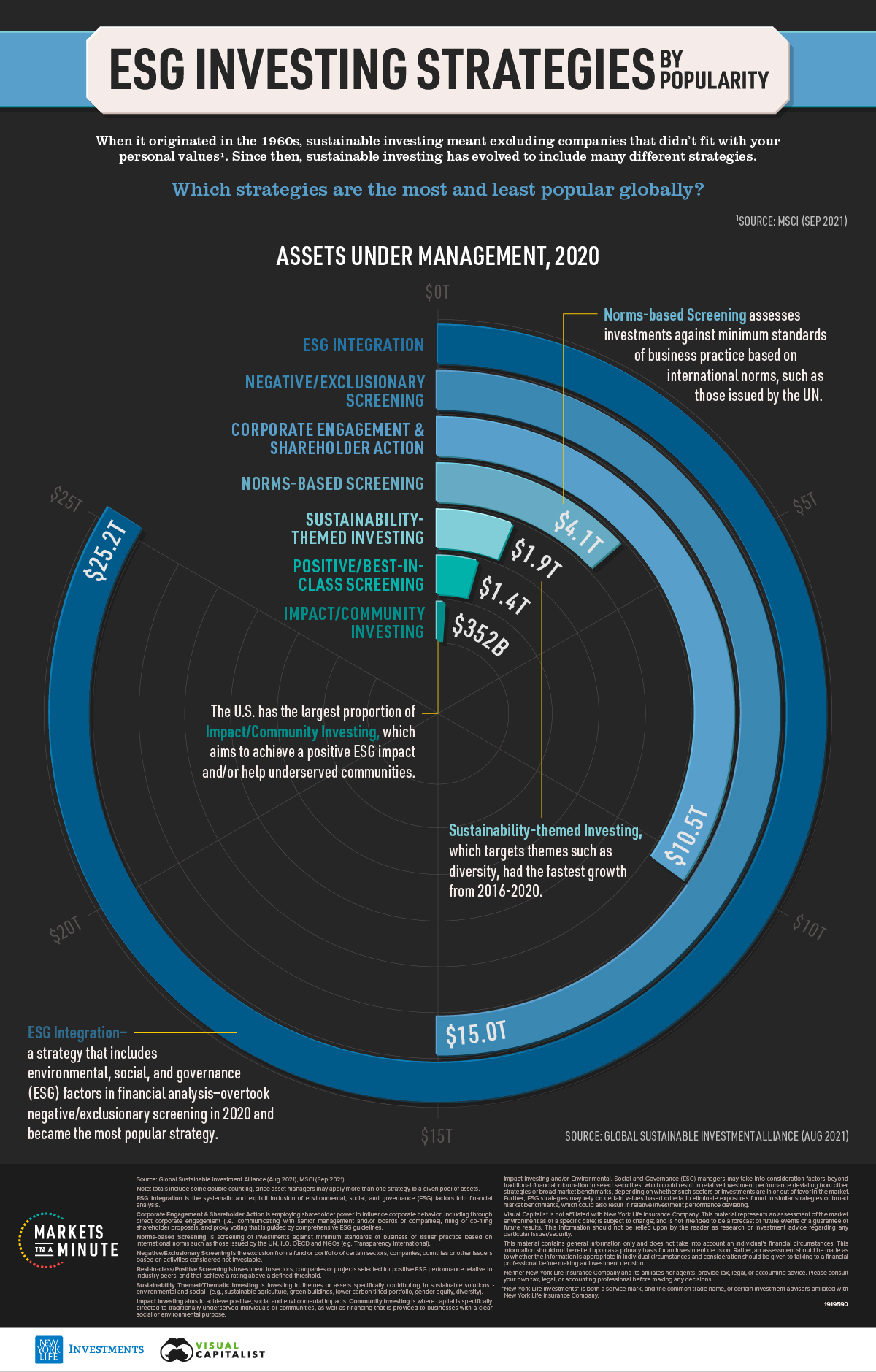

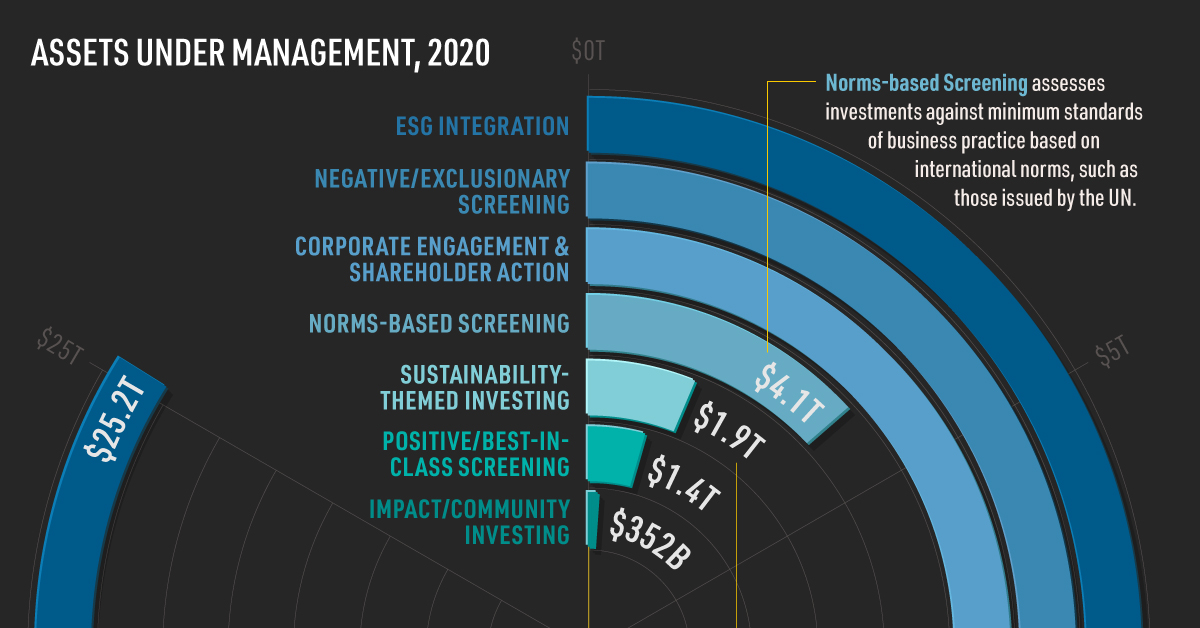

Sustainable Investing Strategies by Global AUM

Below, we show the global assets under management (AUM) of the sustainable investing strategies in 2020. It should be noted that these numbers include some double counting, as asset managers may apply more than one strategy to a given pool of assets.

| Strategy | Global Assets Under Management (2020) |

|---|---|

| ESG integration | $25.2T |

| Negative/exclusionary screening | $15.0T |

| Corporate engagement and shareholder action | $10.5T |

| Norms-based screening | $4.1T |

| Sustainability-themed investing | $1.9T |

| Positive/best-in-class screening | $1.4T |

| Impact/community investing | $352B |

In 2020, ESG integration overtook negative/exclusionary screening to become the most popular of all sustainable investing strategies. Its rise can likely be attributed to having access to more specific data, such as ESG ratings, that make an inclusive approach easier to implement. In addition, many investors are beginning to understand that considering ESG factors alongside financial analysis may help manage investment risks and increase return potential.

Coming in at third place, corporate engagement and shareholder action has over $10 trillion in assets worldwide. A separate report found that the number of ESG-related campaigns went up in 2021, and the success of investor activist campaigns increased slightly year over year. In fact, 25% of surveyed U.S. boards say they have already tied executive compensation to ESG metrics or are planning to do so.

Impact/community investing has the least AUM globally. It is most popular in the U.S., where 60% of the strategy’s total assets are held.

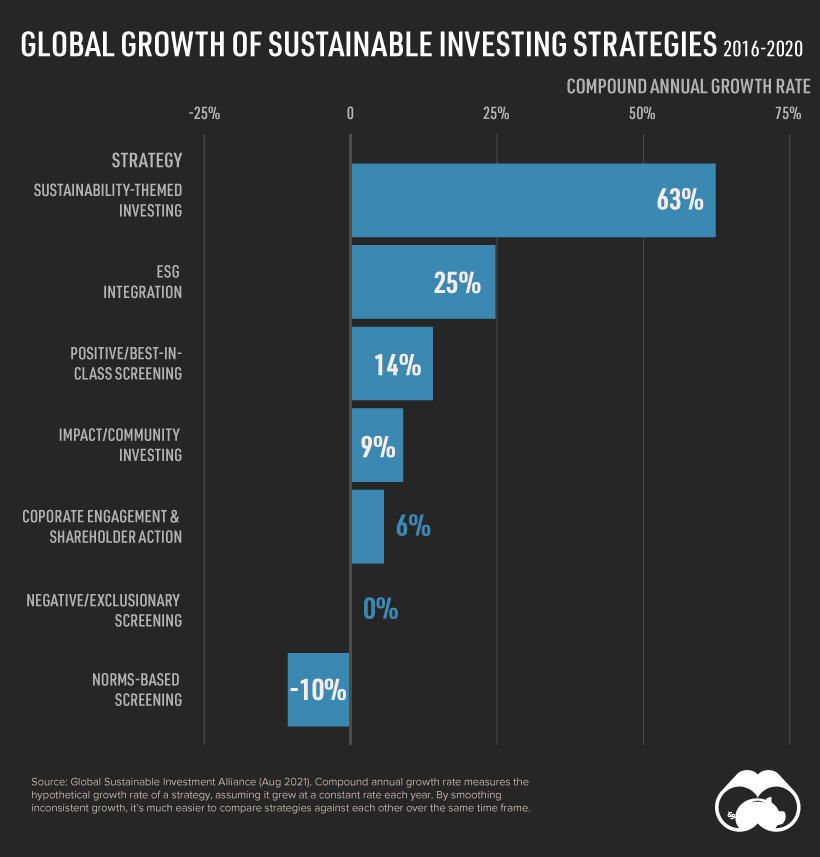

Growth Rate by Strategy

Of course, the above data reflects that some strategies–like exclusionary screening–have been around for longer periods of time. In contrast, the idea of impact investing was spurred in 2009 after the Global Impact Investing Network was launched.

Another way of gauging each strategy’s popularity would be to look at its recent growth. Here’s the compound annual growth rate of the sustainable investing strategies from 2016-2020.

Sustainability-themed investing saw the highest growth. In 2020, it overtook positive/best-in-class screening to become the fifth most popular strategy. This growth mirrors the rise of thematic investing more broadly, as investors aim to capitalize on long-term structural shifts.

Norms-based screening was the only strategy to see negative growth, likely due to the way it is defined. Some standards falling under this strategy are now minimum and mandatory requirements by various national governments, especially in Europe where regulations have tightened. Because it is expected that these regulations are being followed, investors are least likely to say that norms-based screening is the strategy they use when they classify their sustainable investments.

Spoilt for Choice

Compared to the 1960s, today’s investors have many more sustainable investing strategies at their fingertips. However, with more options comes a new challenge: which strategies should investors consider?

The answer will depend on an investor’s objectives, but this data can give some insight on how other investors are approaching sustainable investing.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: Global Macroeconomic Risk, by Country in 2022