Markets in a Minute

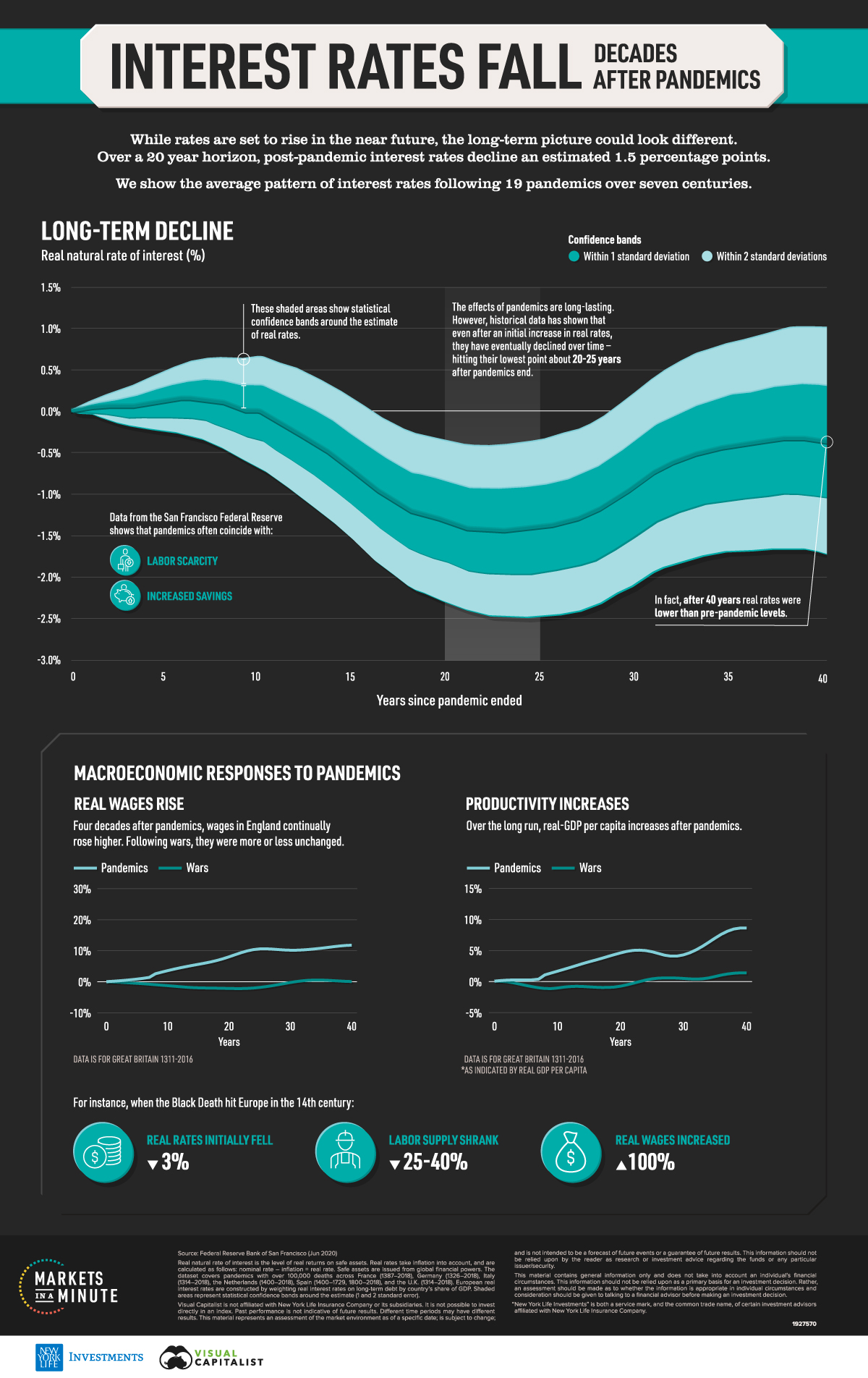

Chart: Interest Rates Fall Decades After Pandemics

This infographic is available as a poster.

This infographic is available as a poster.

Chart: Interest Rates Fall Decades After Pandemics

How have interest rates responded to pandemics?

Despite higher interest rates on the horizon, historical data shows that real interest rates fall decades after pandemics end. Real interest rates were shown to decline as much as 1.5% lower, even after an initial rise.

In this Markets in a Minute chart from New York Life Investments, we show how pandemics have impacted real interest rates across 19 pandemics since the 14th century.

Pandemics and Real Interest Rates

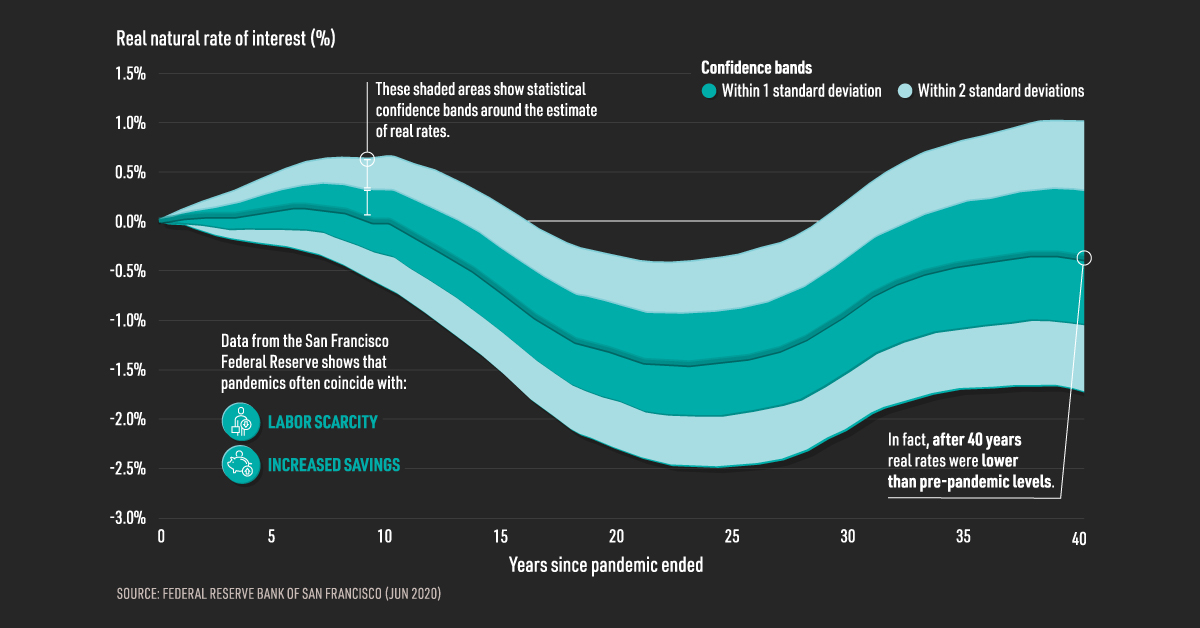

According to a working paper from the San Francisco Federal Reserve Bank, pandemics have lasting effects on real interest rates.

Real rates were defined as the level of returns on safe assets issued from global financial powers.

Specifically, interest rates were constructed by weighting real interest rates on long-term debt by each country’s share of GDP. Data was collected over seven centuries for pandemics with over 100,000 deaths across Europe due to available historical records.

To study how interest rates respond to major economic events over the long run, pandemics were compared to wars.

| Changes in Real Rate | 0 Years | 10 Years | 20 Years | 30 Years | 40 Years |

|---|---|---|---|---|---|

| Pandemics | -0.1% | -0.6% | -1.3% | -1.0% | -0.7% |

| Wars | -0.1% | 0.3% | 0.8% | 0.8% | 0.5% |

Based on their research, interest rates fell slightly after pandemics, but this effect increased over time. What’s more, four decades after pandemics ended, real interest remained lower than pre-pandemic levels. By contrast, interest rates increased after wars, hitting the highest point two to three decades out.

What factors may have impacted a depression in real rates after pandemics?

An abundance of capital per unit of labor was one possible factor. Higher levels of precautionary savings was another, which may be a result of rebuilding lost wealth during the pandemic. According to economic theory, increased savings and a slowing population can lead real interest rates to decline.

In other words, when there is excess capital and people are saving money, there is less demand for credit. This decreased demand, in turn, may lead to lower interest rates.

By contrast, capital is destroyed during wars, which may have caused an upward pressure on rates in the past.

Pandemics vs. Recession Savings

How do savings during pandemics compare to recessions? In April 2020, personal savings rates skyrocketed to over 33%—the highest ever recorded.

In the table below, we show the peak savings rate during the pandemic, and compare it to different recessions.

| Date | Peak Savings Rate |

|---|---|

| Apr 2020 | 33.8% |

| May 2009 | 7.9% |

| Sep 2001 | 7.0% |

| Jan 1991 | 9.3% |

| Nov 1981 | 13.2% |

| Jul 1980 | 11.2% |

| Dec 1973 | 14.8% |

| Jul 1970 | 13.5% |

| Jan 1961 | 11.1% |

Source: U.S. Bureau of Economic Analysis (Jan 2022)

At one point, savings rates during the COVID-19 pandemic were double or triple the rate of past recessions. The average U.S. personal savings rate over the last 60 years is around 9%.

Rise in Real Wages

Like interest rates, real wages showed a meaningful response to pandemics. As labor scarcity increased, real wages rose higher. Overall, pandemics corresponded with a rise in real wages that lasted for decades. For wars, real wages decreased persistently for years.

During the Black Death, for instance, a 25-40% decline in the labor supply corresponded with a 100% rise in real wages.

| Changes in Real Wages in Great Britain | 0 Years | 10 Years | 20 Years | 30 Years | 40 Years |

|---|---|---|---|---|---|

| Pandemics | 0.5% | 3.6% | 8.0% | 10.2% | 11.8% |

| Wars | -0.2% | -1.3% | -2.2% | -2.2% | 0.1% |

It’s worth noting that the study was released in June 2020, long before current wage rises began to appear.

Productivity Increases

Pandemics have also positively impacted productivity. While real GDP per capita rose 8.6% four decades after pandemics, for wars, productivity increased just 1.4%.

| Changes in Real GDP per Capita in Great Britain | 0 Years | 10 Years | 20 Years | 30 Years | 40 Years |

|---|---|---|---|---|---|

| Pandemics | 0.1% | 1.7% | 4.6% | 4.3% | 8.6% |

| Wars | 0.1% | -1.0% | -0.7% | 0.5% | 1.4% |

Why did productivity improve? As the number of workers declined, capital per worker increased, raising labor productivity. In other words, there was more capital available for the remaining workers, boosting productivity.

By contrast, wars have hurt productivity due to the destruction of physical capital such as public infrastructure.

What if COVID-19 Is Different?

Two caveats may impact how real interest rates respond to the current pandemic, according to the research.

In the past, pandemics created a significant dent in the labor force. COVID-19, in comparison, has a greater impact on an elderly demographic in terms of deaths, who are less likely to be in the workforce. As a result, the decrease in capital to labor could depress interest rates to a lesser degree.

Secondly, the fiscal response to COVID-19 is much larger than past pandemics. A major fiscal response could lead to higher debt levels, which in turn could push real interest rates higher. As the central bank prints more money, this could lead to inflation, which causes bonds to be worth less. In turn, investors begin selling bonds and yields rise.

World War II: A Modern Day Case Study

However, there is a case to be made for lower rates for longer.

In the aftermath of World War II, the Federal Reserve sustained low borrowing costs in spite of a soaring economy and high inflation. The central bank kept long-term Treasury yields at 2.5% after the war to stabilize markets and keep government debt financing low. Even amid high debt levels, the debt-to-GDP ratio declined without causing damaging effects on the economy.

Overall, if history repeats itself, there could be a low interest rate environment for a significant period of time, with sustained effects on real wages and productivity.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators