Markets in a Minute

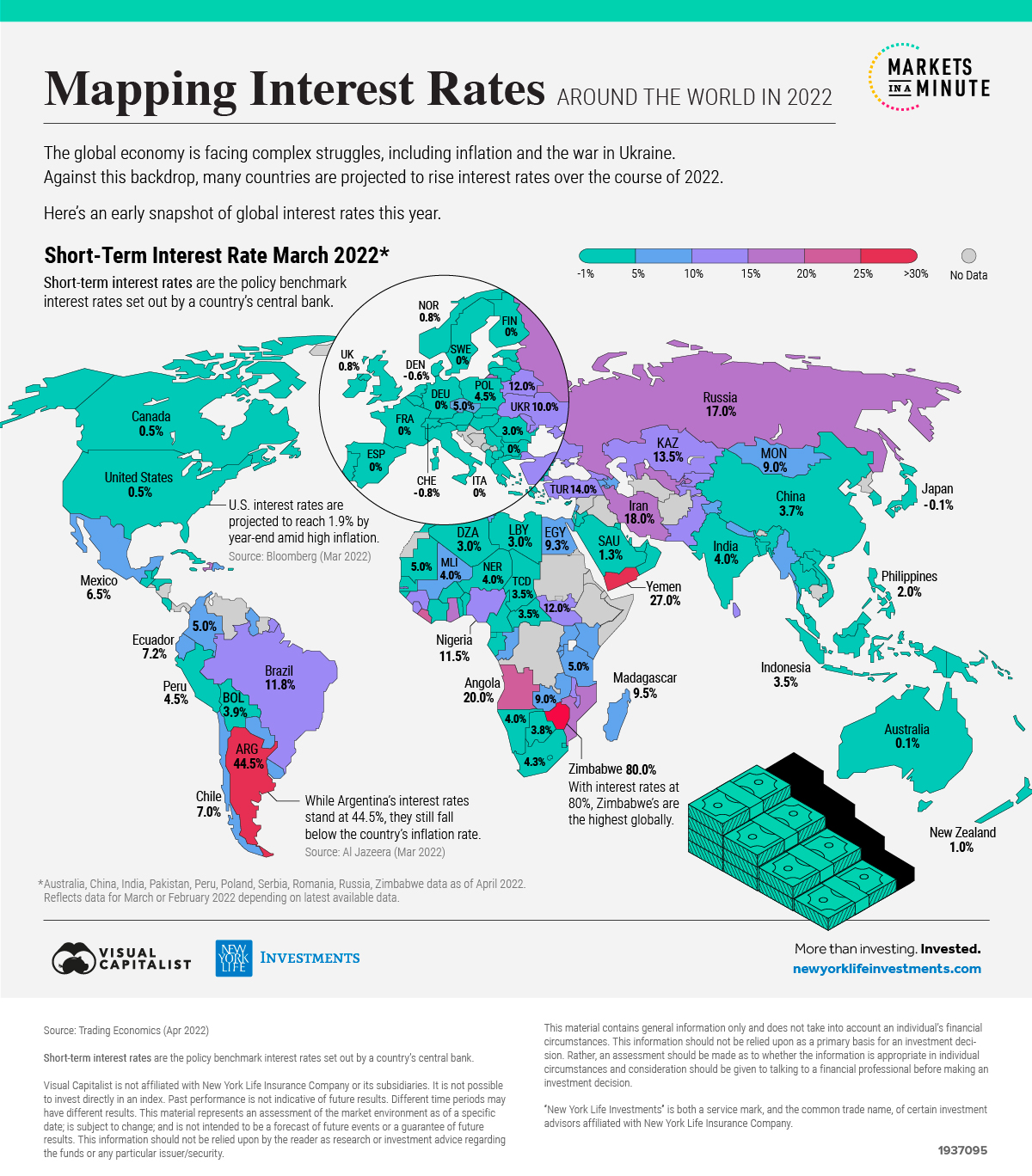

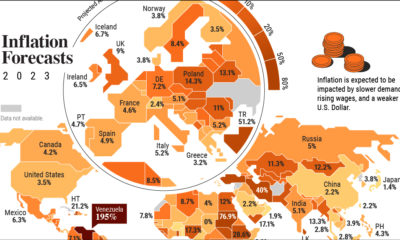

Mapped: Interest Rates by Country in 2022

This infographic is available as a poster.

This infographic is available as a poster.

Mapped: Interest Rates by Country

Soaring inflation, the war in Ukraine, and strengthening economies are spurring interest rate increases around the world. At the same time, central banks are unwinding record monetary stimulus from COVID-19.

In this Markets in a Minute from New York Life Investments, we show interest rates by country in 2022. Interest rates are based on short-term benchmark policy rates set out by central banks.

Interest Rates Around the World in 2022

While the vast majority of countries saw a decline in interest rates over recent years, this trend is reversing for many in 2022.

After hovering at 0.0%, the U.S. increased its short-term interest rate to 0.5%. Experts project up to seven interest rate hikes this year, with interest rates rising as high as 1.9% by year-end.

For many countries in Europe, interest rates climbed out of negative territory for the first time since 2014. Interest rates now sit at 0.0% across the European Union.

| Country/ Region | Short-Term Interest Rate (%) |

|---|---|

| 🇦🇱 Albania | 1.0 |

| 🇦🇲 Armenia | 9.3 |

| 🇦🇺 Australia | 0.1 |

| 🇦🇹 Austria | 0.0 |

| 🇦🇿 Azerbaijan | 7.8 |

| 🇧🇸 Bahamas | 4.0 |

| 🇧🇩 Bangladesh | 4.8 |

| 🇧🇧 Barbados | 2.0 |

| 🇧🇾 Belarus | 12.0 |

| 🇧🇪 Belgium | 0.0 |

| 🇧🇿 Belize | 2.3 |

| 🇧🇴 Bolivia | 3.9 |

| 🇧🇼 Botswana | 3.8 |

| 🇧🇷 Brazil | 11.8 |

| 🇨🇦 Canada | 0.5 |

| 🇹🇩 Chad | 3.5 |

| 🇨🇱 Chile | 7.0 |

| 🇨🇳 China | 3.7 |

| 🇨🇴 Colombia | 5.0 |

| 🇨🇬 Congo | 7.5 |

| 🇨🇷 Costa Rica | 2.5 |

| 🇨🇺 Cuba | 2.3 |

| 🇨🇿 Czech Republic | 5.0 |

| 🇩🇰 Denmark | -0.6 |

| 🇩🇴 Dominican Republic | 5.5 |

| 🇪🇨 Ecuador | 7.2 |

| 🇪🇬 Egypt | 9.3 |

| 🇫🇯 Fiji | 0.3 |

| 🇫🇮 Finland | 0.0 |

| 🇫🇷 France | 0.0 |

| 🇬🇪 Georgia | 11.0 |

| 🇩🇪 Germany | 0.0 |

| 🇬🇷 Greece | 0.0 |

| 🇬🇾 Guyana | 5.0 |

| 🇭🇰 Hong Kong | 0.8 |

| 🇭🇺 Hungary | 4.4 |

| 🇮🇸 Iceland | 2.8 |

| 🇮🇳 India | 4.0 |

| 🇮🇩 Indonesia | 3.5 |

| 🇮🇪 Ireland | 0.0 |

| 🇮🇱 Israel | 0.1 |

| 🇮🇹 Italy | 0.0 |

| 🇯🇲 Jamaica | 4.5 |

| 🇯🇵 Japan | -0.1 |

| 🇯🇴 Jordan | 2.8 |

| 🇰🇿 Kazakhstan | 13.5 |

| 🇰🇪 Kenya | 7.0 |

| 🇰🇬 Kyrgyzstan | 10.0 |

| 🇱🇦 Laos | 3.0 |

| 🇱🇻 Latvia | 0.0 |

| 🇱🇧 Lebanon | 7.8 |

| 🇱🇸 Lesotho | 4.0 |

| 🇱🇾 Libya | 3.0 |

| 🇱🇹 Lithuania | 0.0 |

| 🇱🇺 Luxembourg | 0.0 |

| 🇲🇾 Malaysia | 1.8 |

| 🇲🇻 Maldives | 7.0 |

| 🇲🇱 Mali | 4.0 |

| 🇲🇽 Mexico | 6.5 |

| 🇲🇳 Mongolia | 9.0 |

| 🇲🇦 Morocco | 1.5 |

| 🇳🇵 Nepal | 7.0 |

| 🇳🇱 Netherlands | 0.0 |

| 🇳🇿 New Zealand | 1.0 |

| 🇳🇬 Nigeria | 11.5 |

| 🇳🇴 Norway | 0.8 |

| 🇵🇰 Pakistan | 12.3 |

| 🇵🇾 Paraguay | 6.3 |

| 🇵🇪 Peru | 4.5 |

| 🇵🇭 Philippines | 2.0 |

| 🇵🇱 Poland | 4.5 |

| 🇵🇹 Portugal | 0.0 |

| 🇶🇦 Qatar | 2.5 |

| 🇷🇴 Romania | 3.0 |

| 🇷🇼 Rwanda | 5.0 |

| 🇸🇦 Saudi Arabia | 1.3 |

| 🇷🇸 Serbia | 1.5 |

| 🇸🇱 Sierra Leone | 14.3 |

| 🇸🇬 Singapore | 0.3 |

| 🇸🇰 Slovakia | 0.0 |

| 🇿🇦 South Africa | 4.3 |

| 🇰🇷 South Korea | 1.3 |

| 🇸🇸 South Sudan | 12.0 |

| 🇪🇸 Spain | 0.0 |

| 🇱🇰 Sri Lanka | 13.5 |

| 🇸🇿 Swaziland | 4.0 |

| 🇸🇪 Sweden | 0.0 |

| 🇨🇭 Switzerland | -0.8 |

| 🇹🇼 Taiwan | 1.4 |

| 🇹🇭 Thailand | 0.5 |

| 🇹🇳 Tunisia | 6.3 |

| 🇹🇷 Turkey | 14.0 |

| 🇺🇬 Uganda | 6.5 |

| 🇺🇦 Ukraine | 10.0 |

| 🇦🇪 United Arab Emirates | 1.8 |

| 🇬🇧 United Kingdom | 0.8 |

| 🇺🇸 United States | 0.5 |

| 🇻🇳 Vietnam | 4.0 |

| 🇿🇲 Zambia | 9.0 |

*Australia, China, India, Pakistan, Peru, Poland, Serbia, Romania data as of April 2022.

Reflects data for March or February 2022 depending on latest available data.

Source: Trading Economics (Apr 2022)

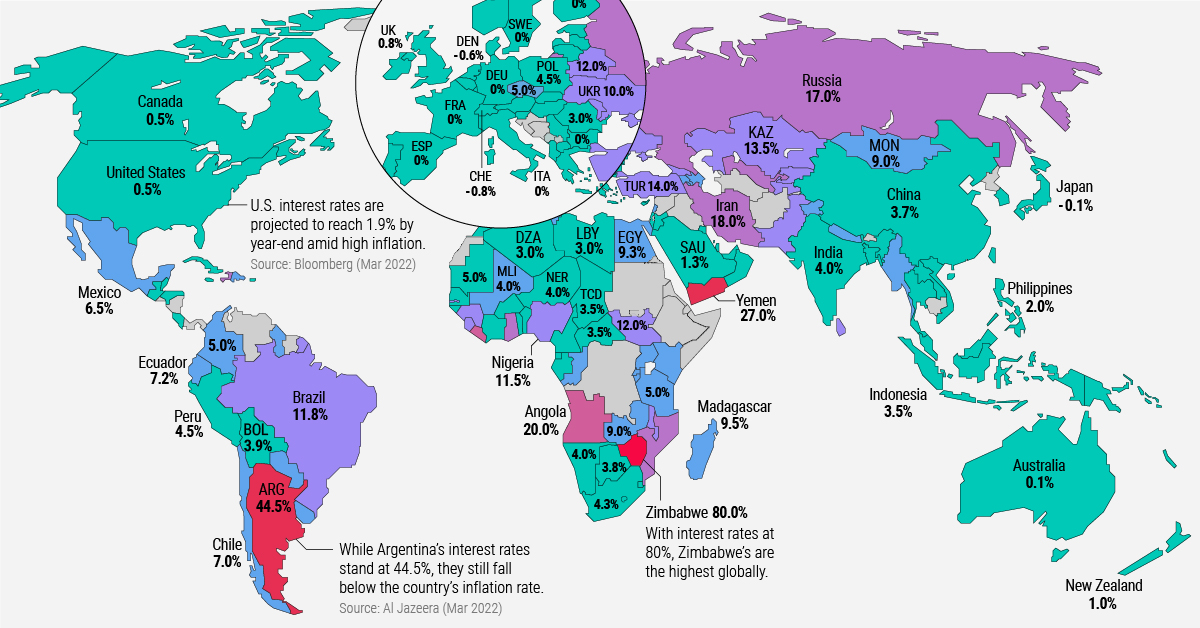

In Latin America, several central banks are taking a hawkish stance as oil price shocks are causing inflation to accelerate.

Mexico raised its benchmark interest rate to 6.5% in March in response to inflation hitting 20-year highs. Even before the war in Ukraine, global factors such as rising oil and import prices were already having a greater impact on Latin American countries than advanced economies.

Unlike the U.S. and most countries located in Europe and Latin America, China is anticipated to potentially lower its interest rates.

A renewed COVID-19 wave has slowed growth, with the government requiring countless factories to close in order to combat the spread of the Omicron variant. Disruptions have cascaded across supply chains—from electric vehicles to iPhones— leaving goods in shorter supply. China is responsible for roughly one-third of global manufacturing.

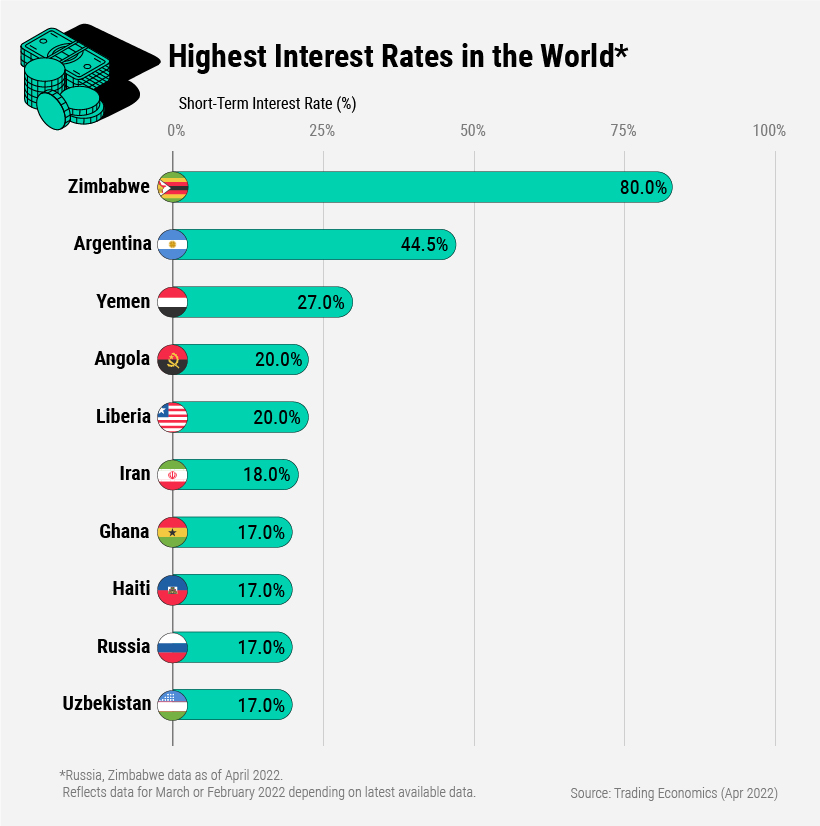

High-Water Mark

Which countries have the highest interest rates in 2022?

At an eye-watering 80%, Zimbabwe has the highest interest rate of any country.

In early April, the central bank raised rates by 20 percentage points to combat a 73% inflation rate. Small businesses, teachers, and analysts have been urging the government to adopt the U.S. dollar to boost economic and investor confidence amid currency woes.

With an interest rate of 44.5%, Argentina has the second-highest rate. To get closer to reaching the requirements for rescheduling its $40 billion loan to the International Monetary Fund (IMF), the central bank raised interest rates for the second time this year. The IMF requires having interest rates above the rate of inflation. As of February, Argentina’s inflation exceeded 50%.

Meanwhile, oil-rich countries such as Angola (20%), Iran (18%), and Russia (17%) all made it into the top 10 for highest rates globally.

Treading Water

What is the outlook for interest rates in 2022 and beyond?

In the short term, experts believe interest rates will likely rise to fight inflation. They could also play a role in slower economic growth, especially if raised too quickly. Recently, the World Bank revised global growth to 3.2% due to the war in Ukraine and rising food and energy prices—about a percentage point lower than its previous forecast of 4.1%.

The longer-term view may look different.

Structural factors, such as an aging population, will likely lead to an increase in savings rates for retirement. In theory, higher savings rates increases the total supply of funds, depressing the interest rate. By 2100, people over 50 are projected to rise from 25% to 40% of the global population.

The end of ultra-low interest rates may be over for now, but broader factors, including growing global debt—which stands at 355% of the world’s GDP—suggests it may be a short to medium-term adjustment.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators