Markets in a Minute

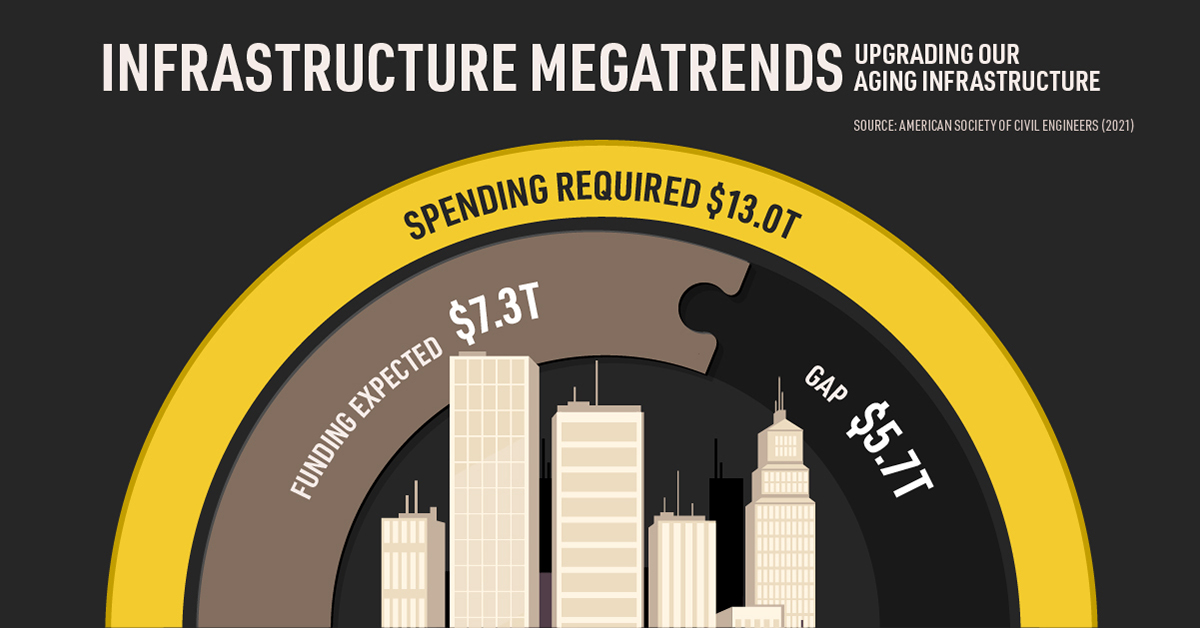

Visualizing the $5.7 Trillion Infrastructure Investment Gap

This infographic is available as a poster.

Infrastructure Megatrends: Filling the Investment Gap

With each passing year, significant investment is required to maintain and improve America’s infrastructure.

When these investments fall behind their targets, an infrastructure gap can emerge. These deficits have a negative impact on the entire American economy, affecting things like roads, highways, water lines, and schools.

In this Markets in a Minute chart from New York Life Investments, we quantify America’s infrastructure gap using research from the American Society of Civil Engineers (ASCE).

The Big Picture

According to ASCE’s 2021 report, $13 trillion in infrastructure spending will be required through 2039 to support America’s economic growth. These projections include the cost of building new infrastructure, as well as the cost of maintaining existing assets.

With expected funding estimated at $7.3 trillion, that leaves a deficit of $5.7 trillion.

If this gap is not filled, the ASCE warns there will be widespread consequences. Goods are likely to become more expensive to produce and transport, resulting in higher costs for consumers. Higher costs could also reduce the international competitiveness of American companies.

The table below outlines some of the most critical findings from the ASCE’s research.

| Costs Associated with the Infrastructure Gap, by 2039 | Details |

|---|---|

| $23 trillion in lost business productivity |

|

| $10 trillion loss in GDP |

|

| $2.4 trillion in lost exports |

|

*Federal Communications Commission

For the average American household, these impacts could lead to a $3,300 decrease in annual disposable income.

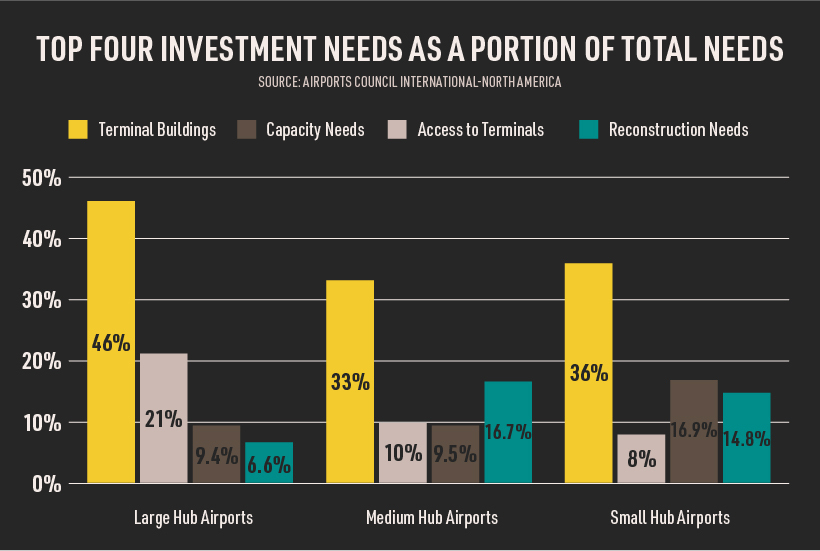

Aviation: A Critical Need for Investment

U.S. airports are facing mounting capacity challenges as more people travel each year (this trend has taken a pause during the COVID-19 pandemic).

Over a two-year period ending in 2019, traffic through America’s airports grew 24% to reach 1.2 billion passengers per year. On the supply side, flight service increased by just 5%. Altogether, insufficient aviation infrastructure resulted in a total of 96 million delay minutes in 2019, up from 66 million in 2017.

The following chart shows a breakdown of how U.S. aviation investment would need to be distributed.

The Federal Aviation Administration estimates that the capital needs for terminal buildings is already more than $6.6 billion.

How Investors Can Benefit

Efforts to address the infrastructure gap are gaining steam—Democrats and Republicans recently joined together to pass a $1 trillion infrastructure bill—but this won’t be enough to fill the gap completely. Nor will it secure the future of the America’s infrastructure.

The good news is that publicly listed infrastructure companies can play a significant role. As owners of essential long-duration assets, these businesses are investing billions annually into upgrades and expansions.

For investors, this supports consistent organic growth and steady income. Analysis by CBRE Clarion Securities determined that income growth has accounted for 50% of listed infrastructure’s total return over the past 20 years.

Income-seeking investors may also find the sector’s defensive characteristics to be attractive. CBRE’s analysis found that listed infrastructure has captured just 65% of the global equity market downside, compared to 81% of the upside.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators