Markets in a Minute

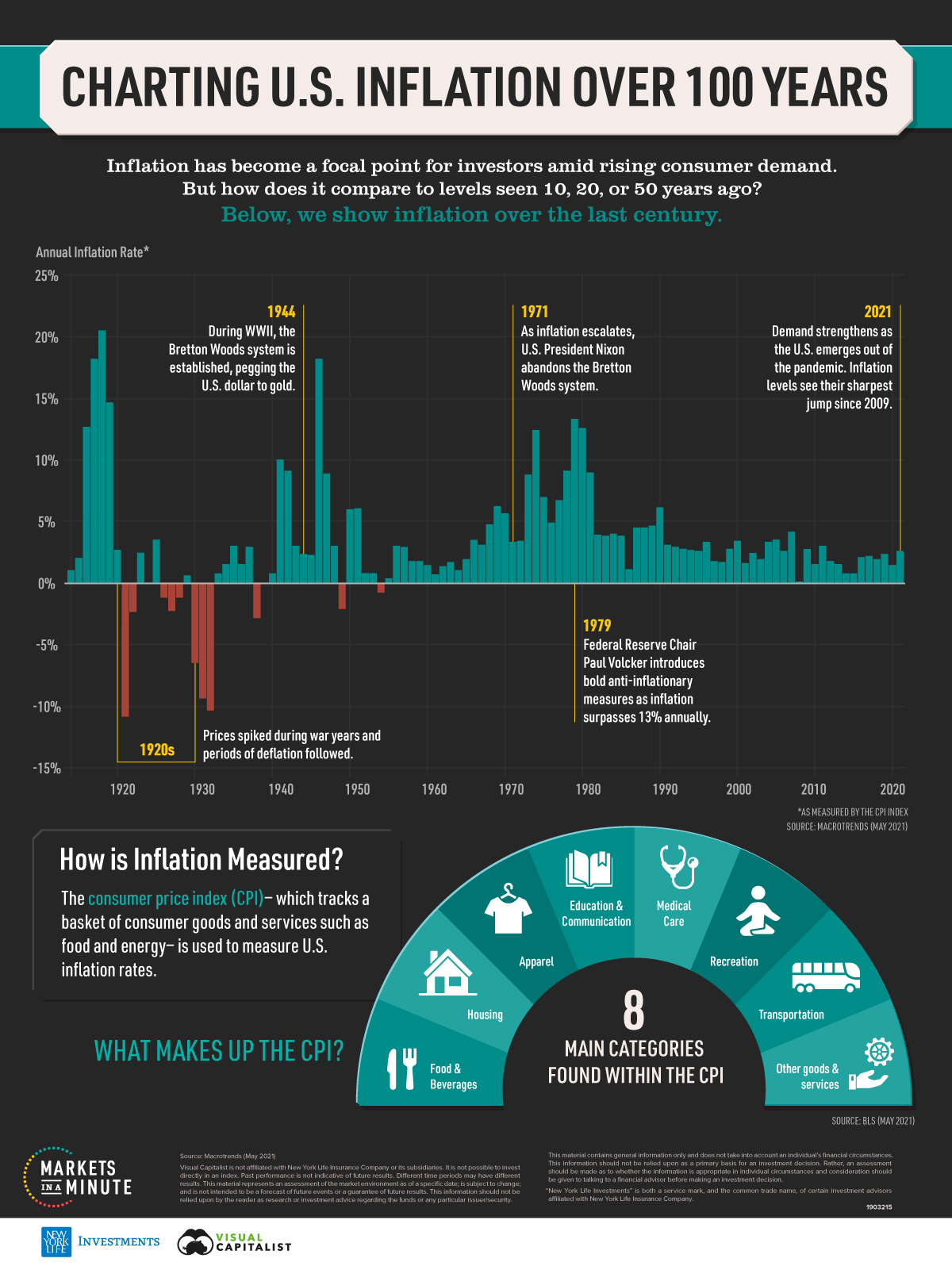

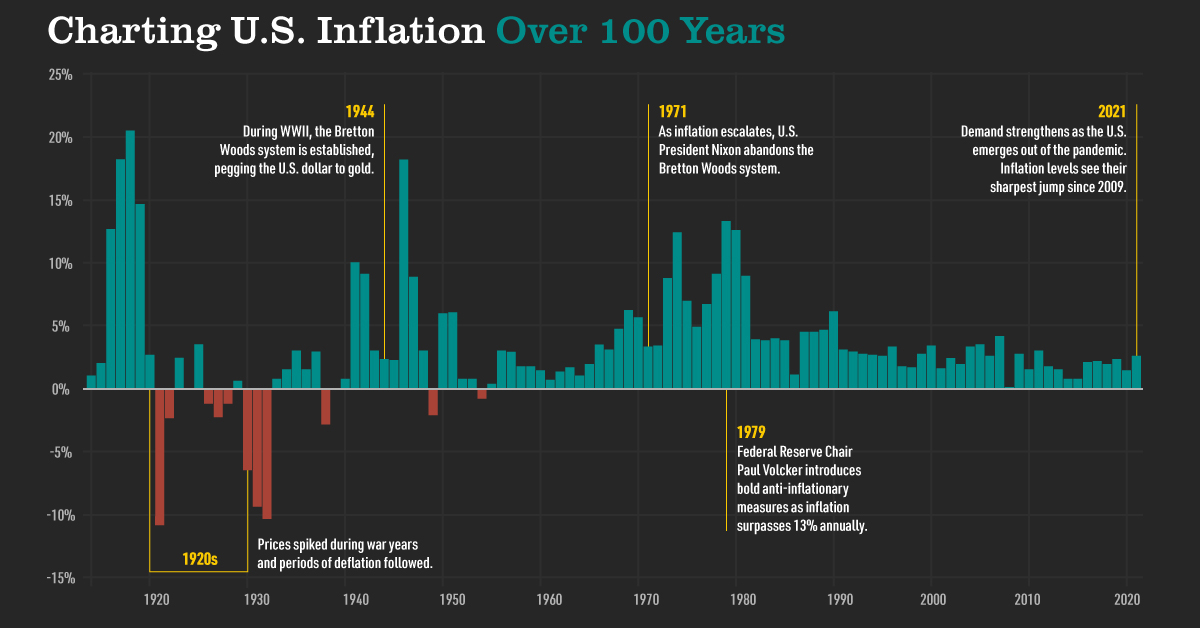

Visualizing the History of U.S. Inflation Over 100 Years

This infographic is available as a poster.

This infographic is available as a poster.

Visualizing the History of U.S. Inflation Over 100 Years

Is inflation rising?

The consumer price index (CPI), an index used as a proxy for inflation in consumer prices, offers some answers. In 2020, inflation dropped to 1.4%, the lowest rate since 2015. By comparison, inflation sits around 2.5% as of June 2021.

For context, recent numbers are just above rates seen in 2019, which were 2.3%. Given how the economic shock of COVID-19 depressed prices, rising price levels make sense. However, other variables, such as a growing money supply and rising raw materials costs, could factor into rising inflation.

To show current price levels in context, this Markets in a Minute chart from New York Life Investments shows the history of inflation over 100 years.

U.S. Inflation: Early History

Between the founding of the U.S. in 1776 to the year 1914, one thing was for sure—wartime periods were met with high inflation.

At the time, the U.S. operated under a classical Gold Standard regime, with the dollar’s value tied to gold. During the Civil War and World War I, the U.S. went off the Gold Standard in order to print money and finance the war. When this occurred, it triggered inflationary episodes, with prices rising upwards of 20% in 1918.

| Year | Inflation Rate* |

|---|---|

| 1914 | 1.0% |

| 1915 | 2.0% |

| 1916 | 12.6% |

| 1917 | 18.1% |

| 1918 | 20.4% |

| 1919 | 14.6% |

| 1920 | 2.7% |

| 1921 | -10.8% |

| 1922 | -2.3% |

| 1923 | 2.4% |

| 1924 | 0% |

| 1925 | 3.5% |

| 1926 | -1.1% |

| 1927 | -2.3% |

| 1928 | -1.2% |

| 1929 | 0.6% |

| 1930 | -6.4% |

| 1931 | -9.3% |

| 1932 | -10.3% |

| 1933 | 0.8% |

| 1934 | 1.5% |

| 1935 | 3.0% |

| 1936 | 1.5% |

| 1937 | 2.9% |

| 1938 | -2.8% |

| 1939 | 0.0% |

| 1940 | 0.7% |

| 1941 | 9.9% |

| 1942 | 9.0% |

| 1943 | 3.0% |

| 1944 | 2.3% |

| 1945 | 2.3% |

| 1946 | 18.1% |

| 1947 | 8.8% |

| 1948 | 3.0% |

| 1949 | -2.1% |

| 1950 | 5.9% |

| 1951 | 6.0% |

| 1952 | 0.8% |

| 1953 | 0.8% |

| 1954 | -0.7% |

| 1955 | 0.4% |

| 1956 | 3.0% |

| 1957 | 2.9% |

| 1958 | 1.8% |

| 1959 | 1.7% |

| 1960 | 1.4% |

| 1961 | 0.7% |

| 1962 | 1.3% |

| 1963 | 1.6% |

| 1964 | 1.0% |

| 1965 | 1.9% |

| 1966 | 3.5% |

| 1967 | 3.0% |

| 1968 | 4.7% |

| 1969 | 6.2% |

| 1970 | 5.6% |

| 1971 | 3.3% |

| 1972 | 3.4% |

| 1973 | 8.7% |

| 1974 | 12.3% |

| 1975 | 6.9% |

| 1976 | 4.9% |

| 1977 | 6.7% |

| 1978 | 9.0% |

| 1979 | 13.3% |

| 1980 | 12.5% |

| 1981 | 8.9% |

| 1982 | 3.8% |

| 1983 | 3.8% |

| 1984 | 4.0% |

| 1985 | 3.8% |

| 1986 | 1.1% |

| 1987 | 4.4% |

| 1988 | 4.4% |

| 1989 | 4.7% |

| 1990 | 6.1% |

| 1991 | 3.1% |

| 1992 | 2.9% |

| 1993 | 2.8% |

| 1994 | 2.7% |

| 1995 | 2.5% |

| 1996 | 3.3% |

| 1997 | 1.7% |

| 1998 | 1.6% |

| 1999 | 2.7% |

| 2000 | 3.4% |

| 2001 | 1.6% |

| 2002 | 2.4% |

| 2003 | 1.9% |

| 2004 | 3.3% |

| 2005 | 3.4% |

| 2006 | 2.5% |

| 2007 | 4.1% |

| 2008 | 0.1% |

| 2009 | 2.7% |

| 2010 | 1.5% |

| 2011 | 3.0% |

| 2012 | 1.7% |

| 2013 | 1.5% |

| 2014 | 0.8% |

| 2015 | 0.7% |

| 2016 | 2.1% |

| 2017 | 2.1% |

| 2018 | 1.9% |

| 2019 | 2.3% |

| 2020 | 1.4% |

| 2021 | 2.5% |

Source: Macrotrends (June, 2021)

*As measured by the Consumer Price Index (CPI)

However, when the government returned to a modified Gold Standard, deflationary periods followed, leading prices to effectively stabilize, on average, leading up to World War II.

The Move to Bretton Woods

Like post-World War I, the Great Depression of the 1930s coincided with deflationary pressures on prices. Due to the rigidity of the monetary system at the time, countries had difficulty increasing money supply to help boost their economy. Many countries exited the Gold Standard during this time, and by 1933 the U.S. abandoned it completely.

A decade later, with the Bretton Woods Agreement in 1944, global currency exchange values pegged to the dollar, while the dollar was pegged to gold. The U.S. held the majority of gold reserves, and the global reserve currency transitioned from the sterling pound to the dollar.

1970’s Regime Change

By 1971, the ability for gold to cover the supply of U.S. dollars in circulation became an increasing concern.

Leading up to this point, a surplus of money supply was created due to military expenses, foreign aid, and others. In response, President Richard Nixon abandoned the Bretton Woods Agreement in 1971 for a floating exchange, known as the “Nixon shock”. Under a floating exchange regime, rates fluctuate based on supply and demand relative to other currencies.

A few years later, oil shocks of 1973 and 1974 led inflation to soar past 12%. By 1979, inflation surged in excess of 13%.

The Volcker Era

In 1979, Federal Reserve Chair Paul Volcker was sworn in, and he introduced stark changes to combat inflation that differed from previous regimes.

Instead of managing inflation through interest rates, which the Federal Reserve had done previously, inflation would be managed through controlling the money supply. If the money supply was limited, this would cause interest rates to increase.

While interest rates jumped to 20% in 1980, by 1983 inflation dropped below 4% as the economy recovered from the recession of 1982, and oil prices rose more moderately. Over the last four decades, inflation levels have remained relatively stable since the measures of the Volcker era were put in place.

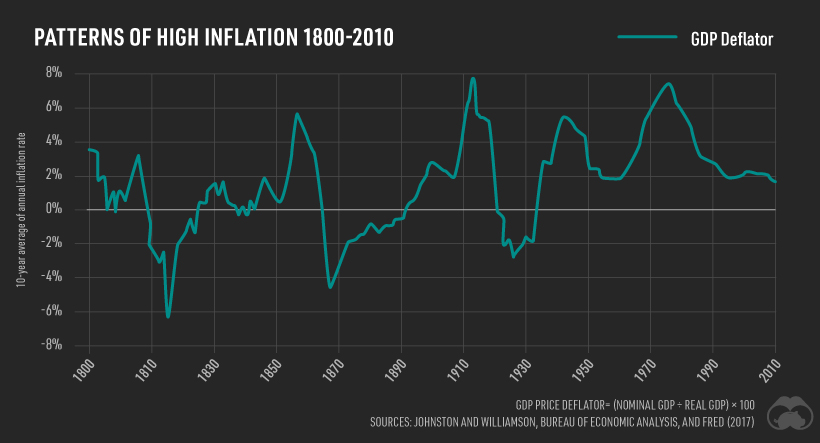

Fluctuating Prices Over History

Throughout U.S. history. there have been periods of high inflation.

As the chart below illustrates, at least four distinct periods of high inflation have emerged between 1800 and 2010. The GDP deflator measurement shown accounts for the price change of all of an economy’s goods and services, as opposed to the CPI index which is a fixed basket of goods.

It is measured as GDP Price Deflator = (Nominal GDP ÷ Real GDP) × 100.

According to this measure, inflation hit its highest levels in the 1910s, averaging nearly 8% annually over the decade. Between 1914 and 1918 money supply doubled to finance war efforts, compared to a 25% increase in GDP during this period.

U.S. Inflation: Present Day

As the U.S. economy reopens, consumer demand has strengthened.

Meanwhile, supply bottlenecks, from semiconductor chips to lumber, are causing strains on automotive and tech industries. While this points towards increasing inflation, some suggest that it may be temporary, as prices were depressed in 2020.

At the same time, the Federal Reserve is following an “average inflation targeting” regime, which means that if a previous inflation shortfall occurred in the previous year, it would allow for higher inflationary periods to make up for them. As the last decade has been characterized by low inflation and low interest rates, any prolonged period of inflation will likely have pronounced effects on investors and financial markets.

Markets in a Minute

The Top 5 Reasons Clients Fire a Financial Advisor

Firing an advisor is often driven by more than cost and performance factors. Here are the top reasons clients ‘break up’ with their advisors.

The Top 5 Reasons Clients Fire a Financial Advisor

What drives investors to fire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for firing a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients fire an advisor to provide insight on what’s driving investor behavior.

What Drives Firing Decisions?

Here are the top reasons clients terminated their advisor, based on a survey of 184 respondents:

| Reason for Firing | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Quality of financial advice and services | 32% | Emotion-based reason |

| Quality of relationship | 21% | Emotion-based reason |

| Cost of services | 17% | Financial-based reason |

| Return performance | 11% | Financial-based reason |

| Comfort handling financial issues on their own | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While firing an advisor is rare, many of the primary drivers behind firing decisions are also emotionally driven.

Often, advisors were fired due to the quality of the relationship. In many cases, this was due to an advisor not dedicating enough time to fully grasp their personal financial goals. Additionally, wealthier, and more financially literate clients are more likely to fire their advisors—highlighting the importance of understanding the client.

Key Takeaways

Given these driving factors, here are five ways that advisors can build a lasting relationship through recognizing their clients’ emotional needs:

- Understand your clients’ deeper goals

- Reach out proactively

- Act as a financial coach

- Keep clients updated

- Conduct goal-setting exercises on a regular basis

By communicating their value and setting expectations early, advisors can help prevent setbacks in their practice by adeptly recognizing the emotional motivators of their clients.

Markets in a Minute

The Top 5 Reasons Clients Hire a Financial Advisor

Here are the most common drivers for hiring a financial advisor, revealing that investor motivations go beyond just financial factors.

The Top 5 Reasons Clients Hire a Financial Advisor

What drives investors to hire a financial advisor?

From saving for a down payment to planning for retirement, clients turn to advisors to guide them through life’s complex financial decisions. However, many of the key reasons for hiring a financial advisor stem from emotional factors, and go beyond purely financial motivations.

We partnered with Morningstar to show the top reasons clients hire a financial advisor to provide insight on what’s driving investor behavior.

What Drives Hiring Decisions?

Here are the most common reasons for hiring an advisor, based on a survey of 312 respondents.

| Reason for Hiring | % of Respondents Citing This Reason | Type of Motivation |

|---|---|---|

| Specific goals or needs | 32% | Financial-based reason |

| Discomfort handling finances | 32% | Emotion-based reason |

| Behavioral coaching | 17% | Emotion-based reason |

| Recommended by family or friends | 12% | Emotion-based reason |

| Quality of relationship | 10% | Emotion-based reason |

Numbers may not total 100 due to rounding. Respondents could select more than one answer.

While financial factors played an important role in hiring decisions, emotional reasons made up the largest share of total responses.

This illustrates that clients place a high degree of importance on reaching specific goals or needs, and how an advisor communicates with them. Furthermore, clients seek out advisors for behavioral coaching to help them make informed decisions while staying the course.

Key Takeaways

With this in mind, here are five ways advisors can provide value to their clients and grow their practice:

- Address clients’ emotional needs early on

- Demonstrate how you can offer support

- Use ordinary language

- Provide education to help clients stay on track

- Acknowledge that these are issues we all face

By addressing emotional factors, advisors can more effectively help clients’ navigate intricate financial decisions and avoid common behavioral mistakes.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators