Infographics

How to Optimize Retirement Plan Design for Your Client

This infographic is available as a poster.

This infographic is available as a poster.

How to Optimize Retirement Plan Design for Your Client

More than ever, retirement plans are looking at an employee’s entire retirement picture.

In line with this trend, advisors are offering personalized services to help people reach their goals. But as retirement plans begin to expand their products and services, unidentified gaps remain in employees’ retirement needs.

To help advisors identify these disconnects, this infographic from New York Life Investments shows the key priorities across both employees and their employers to help optimize retirement plan design.

Are People Achieving Their Retirement Vision?

Today, retirement is an issue that can no longer be ignored.

Nearly 70% of Americans say the country faces a retirement crisis and 54% are worried about a financially secure retirement. Making matters worse, the pandemic has led one in three workers to rethink their retirement timeline.

To look deeper into retirement plan design, NYL Investments partnered with RTI Research, surveying 800 people:

- 500 Plan Participants: Employees with 401(k)/ 403(b) plans

- 150 Plan Sponsors: Companies offering 401(k) plans

- 150 Plan Providers: Advisors providing 401(k) services

Here are the results they found.

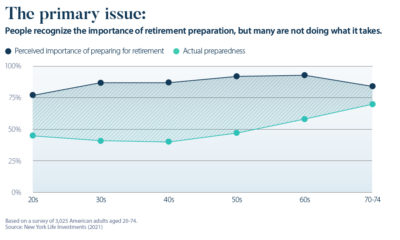

Preparedness for Retirement

Two structural trends—lack of savings and not having access to a retirement plan at work—are impacting retirement readiness today.

By a significant margin, the survey found that men (45%) feel more prepared for retirement than women (30%), which may be explained by historically higher earnings.

How does retirement preparedness break down by age group?

| Age | Very Well Prepared | Somewhat Prepared | Not Very Well Prepared |

|---|---|---|---|

| 20s | 45% | 23% | 21% |

| 30s | 42% | 44% | 14% |

| 40s | 30% | 41% | 29% |

| 50s | 34% | 38% | 28% |

| 60s | 37% | 53% | 9% |

| Average | 37% | 42% | 21% |

On average, 37% of employees felt very prepared. Despite those in their 40s often hitting their highest-earning potential, employees in this age bracket felt the least prepared.

Retirement Plan Features

What aspects of their retirement plan did survey participants feel very satisfied with?

| Feature | % Who Feel Very Satisfied | Somewhat Prepared | Not Very Well Prepared |

|---|---|---|---|

| Employer commitment to retirement preparedness | 58% | 23% | 21% |

| Plan provider | 62% | 44% | 14% |

| Plan performance | 58% | 41% | 29% |

| Ease of account management | 66% | 38% | 28% |

| Number of investment options given | 58% | 53% | 9% |

Compared to other variables, participants felt most satisfied with the ease of account management of their retirement plan along with their plan provider.

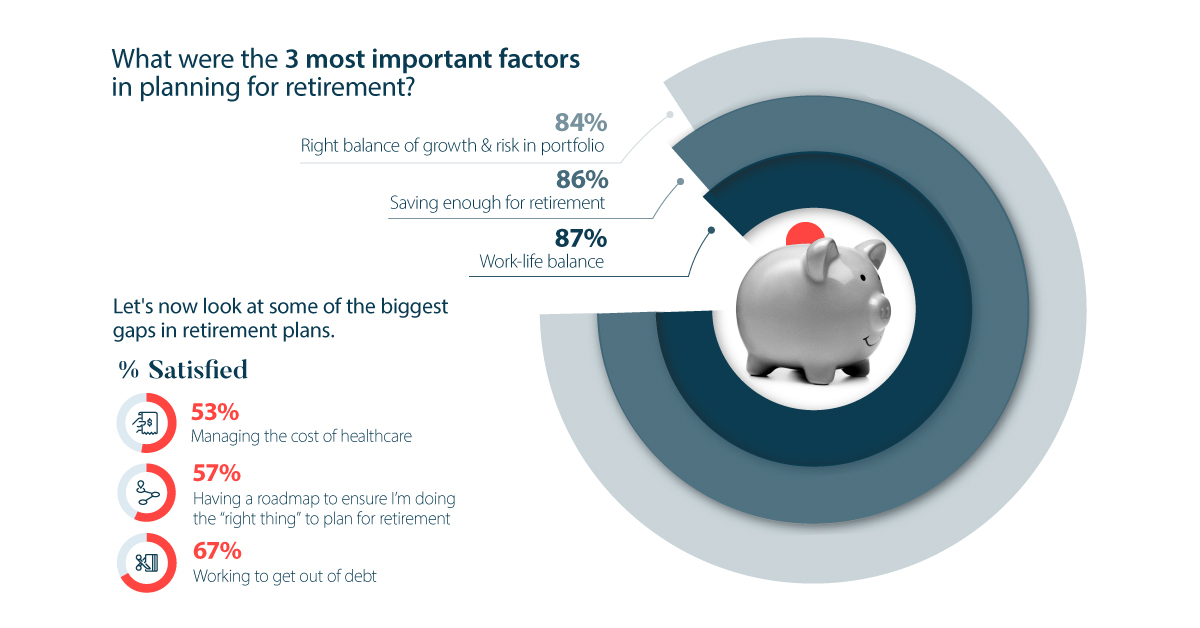

Retirement Plan Design: 3 Key Priorities

When it comes to actual planning for retirement, what were the three most important factors among participants?

- Right balance of growth & risk in portfolio: 84%

- Saving enough for retirement: 86%

- Work-life balance: 87%

Interestingly, the importance of work-life balance increased with age.

While 78% of people in their 20s said this was very important, it increased to 92% of people in their 50s. The same pattern emerged for having enough savings for retirement. Over 75% of people in their 20s said this was extremely important. For those in their 50s, this jumped to 96%.

Retirement Plan Design: 3 Gaps

Let’s now look at some of the biggest gaps in retirement plan design. Here is where participants were least satisfied with their plan provider:

| Service | % Satisfied |

|---|---|

| Managing the cost of healthcare | 53% |

| Having a roadmap to ensure I’m doing the “right thing” to plan for retirement | 57% |

| Working to get out of debt | 67% |

As the above findings suggest, not only are participants looking for guidance with their 401(k) investments, they are looking for personal financial advice on managing debt and healthcare costs.

These gaps make sense: the U.S. has the highest healthcare costs in the world, averaging $12,500 per person per year or three times higher than the OECD country average.

The Employer’s Perspective

Let’s now take a look at how employers viewed retirement plan design.

Retirement Plan Design: Key Priorities

Across all firms, what were the three most important factors for their employees?

- Managing the cost of healthcare: 90%

- Saving enough for retirement: 85%

- Work-life balance: 85%

Both employers and employees alike placed saving enough for retirement near the top.

Retirement Plan Design: 3 Gaps

Which services do employers offer the least?

| Service | % Offered |

|---|---|

| Working to get out of debt | 23% |

| How to access Social Security and other retirement accounts | 33% |

| Saving enough for retirement | 34% |

Interestingly, while 85% of employers place saving enough for retirement as a key priority, the vast majority of employers don’t offer these services in retirement plans.

To address these gaps, advisors can create a well-thought-out financial wellness program for employers that bridges the disconnect.

Understanding the Disconnect

Over the last five years, retirement plans that offer advice have risen 44%.

The evidence is clear: employers value providing their employees personalized advice. Here are some key insights on providers, and where the disconnects lie.

Plan Providers: Key Disconnects

While 93% of all plan providers surveyed offer advisory services, just 62% offered services that were educational.

Meanwhile, younger advisors felt employees had stronger financial literacy and knowledge of retirement services compared to more tenured advisors by a wide margin. A similar trend followed for advisors at smaller plan providers versus larger firms.

However, more tenured advisors at larger firms were more likely to offer in-person consultations at the workplace. The same was true for providing employees with information to make more informed investment decisions.

Next, while some of the largest disconnects from participant and employer needs center around managing debt and healthcare costs, the majority of plan providers don’t offer them:

| 3 Gaps in Providers | % Offer Service |

|---|---|

| Working to get out of debt | 35% |

| Managing cost of healthcare | 29% |

| Work-life balance | 34% |

Importantly, new opportunities arise when advisors connect with participants and employers in areas that matter most.

Optimizing Retirement Plan Design

When employees and sponsors are active participants in their retirement journey, advisors can provide human-centered advice, personalized skills, and holistic planning models.

Based on the above findings, advisors can strategically enhance retirement plan design to align with participants’ and employers’ financial needs.

Infographics

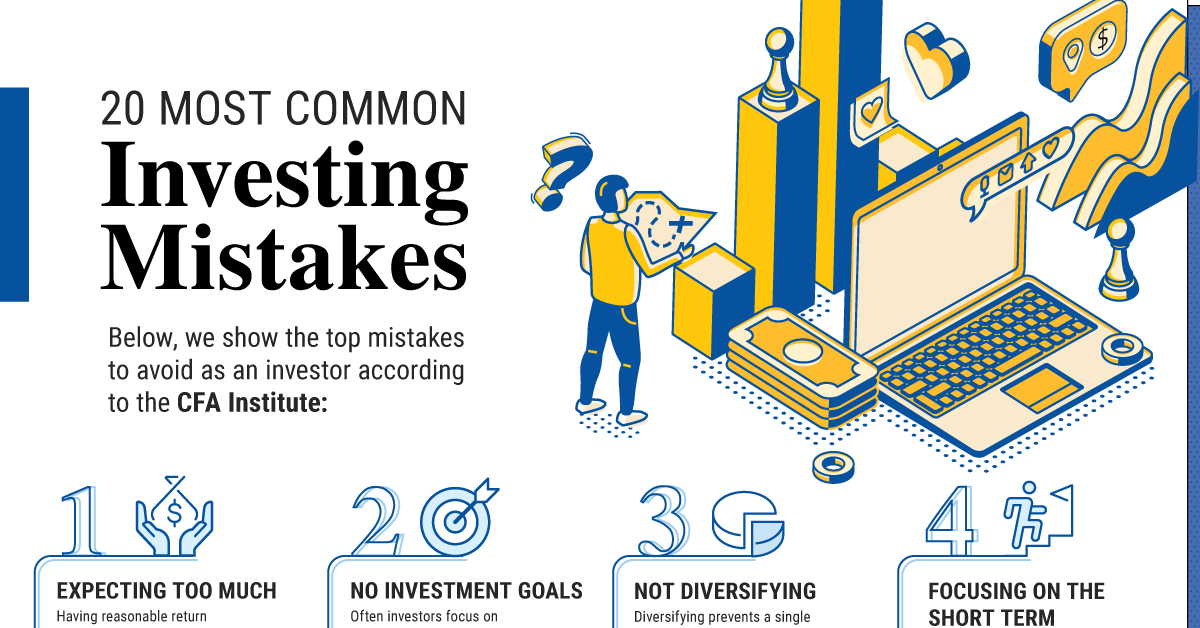

The 20 Most Common Investment Mistakes, in One Chart

Here are the top investment mistakes to avoid, from emotionally driven investing to paying too much in fees.

The 20 Most Common Investment Mistakes

No one is immune to errors, including the best investors in the world.

Fortunately, investment mistakes can provide valuable lessons over time, providing investors an opportunity to gain insights on investing—and build more resilient portfolios.

This graphic shows the top 20 mistakes to watch out for, according to the CFA Institute.

20 Investment Mistakes to Avoid

From emotionally driven investment decisions to paying too much on fees, here are some mistakes that investors commonly make:

| Top 20 Mistakes | Description |

|---|---|

| 1. Expecting Too Much | Having reasonable return expectations helps investors keep a long-term view without reacting emotionally. |

| 2. No Investment Goals | Often investors focus on short-term returns or the latest investment craze instead of their long-term investment goals. |

| 3. Not Diversifying | Diversifying prevents a single stock from drastically impacting the value of your portfolio. |

| 4. Focusing on the Short Term | It’s easy to focus on the short term, but this can make investors second-guess their original strategy and make careless decisions. |

| 5. Buying High and Selling Low | Investor behavior during market swings often hinders overall performance. |

| 6. Trading Too Much | One study shows that the most active traders underperformed the U.S. stock market by 6.5% on average annually. Source: The Journal of Finance |

| 7. Paying Too Much in Fees | Fees can meaningfully impact your overall investment performance, especially over the long run. |

| 8. Focusing Too Much on Taxes | While tax-loss harvesting can boost returns, making a decision solely based on its tax consequences may not always be merited. |

| 9. Not Reviewing Investments Regularly | Review your portfolio quarterly or annually to make sure you’re staying on track or if your portfolio is in need of rebalancing. |

| 10. Misunderstanding Risk | Too much risk can take you out of your comfort zone, but too little risk may result in lower returns that do not reach your financial goals. Recognize the right balance for your personal situation. |

| 11. Not Knowing Your Performance | Often, investors don’t actually know the performance of their investments. Review your returns to track if you are meeting your investment goals factoring in fees and inflation. |

| 12. Reacting to the Media | Negative news in the short-term can trigger fear, but remember to focus on the long run. |

| 13. Forgetting About Inflation | Historically, inflation has averaged 4% annually. Value of $100 at 4% Annual Inflation After 1 Year: $96 After 20 Years: $44 |

| 14. Trying to Time the Market | Market timing is extremely hard. Staying in the market can generate much higher returns versus trying to time the market perfectly. |

| 15. Not Doing Due Diligence | Check the credentials of your advisor through sites like BrokerCheck, which shows their employment history and complaints. |

| 16. Working With the Wrong Advisor | Taking the time to find the right advisor is worth it. Vet your advisor carefully to ensure your goals are aligned. |

| 17. Investing With Emotions | Although it can be challenging, remember to stay rational during market fluctuations. |

| 18. Chasing Yield | High-yielding investments often carry the highest risk. Carefully assess your risk profile before investing in these types of assets. |

| 19. Neglecting to Start | Consider two people investing $200 monthly assuming a 7% annual rate of return until the age of 65. If one person started at age 25, their end portfolio would be $520K, but if the other started at 35 it would total about $245K. |

| 20. Not Controlling What You Can | While no one can predict the market, investors can control small contributions over time, which can have powerful outcomes. |

For instance, not properly diversifying can expose you to higher risk. Holding one concentrated position can drastically impact the value of your portfolio when prices fluctuate.

In fact, one study shows that the optimal diversification for a large-cap portfolio is holding 15 stocks. In this way, it helps capture the highest possible return relative to risk. When it came to a small-cap portfolio, the number of stocks rose to 26 for optimal risk reduction.

It’s worth noting that one size does not fit all, and seeking financial advice can help you find the right balance based on your financial goals.

Another common mistake is trading too much. Since each trade can rake up fees, this can impact your overall portfolio performance. A separate study showed that the most active traders saw the worst returns, underperforming the U.S. stock market by 6.5% on average annually.

Finally, it’s important to carefully monitor your investments regularly as market conditions change, factoring in fees and inflation. This will let you know if your investments are on track, or if you need to adjust based on changing personal circumstances or other factors.

Controlling What You Can

To help avoid these mistakes, investors can remember to stay rational and focus on their long-term goals. Building a solid portfolio often involves assessing the following factors:

- Financial goals

- Current income

- Spending habits

- Market environment

- Expected returns

With these factors in mind, investors can avoid focusing on short-term market swings, and control what they can. Making small investments over the long run can have powerful effects, with the potential to accumulate significant wealth simply by investing consistently over time.

Infographics

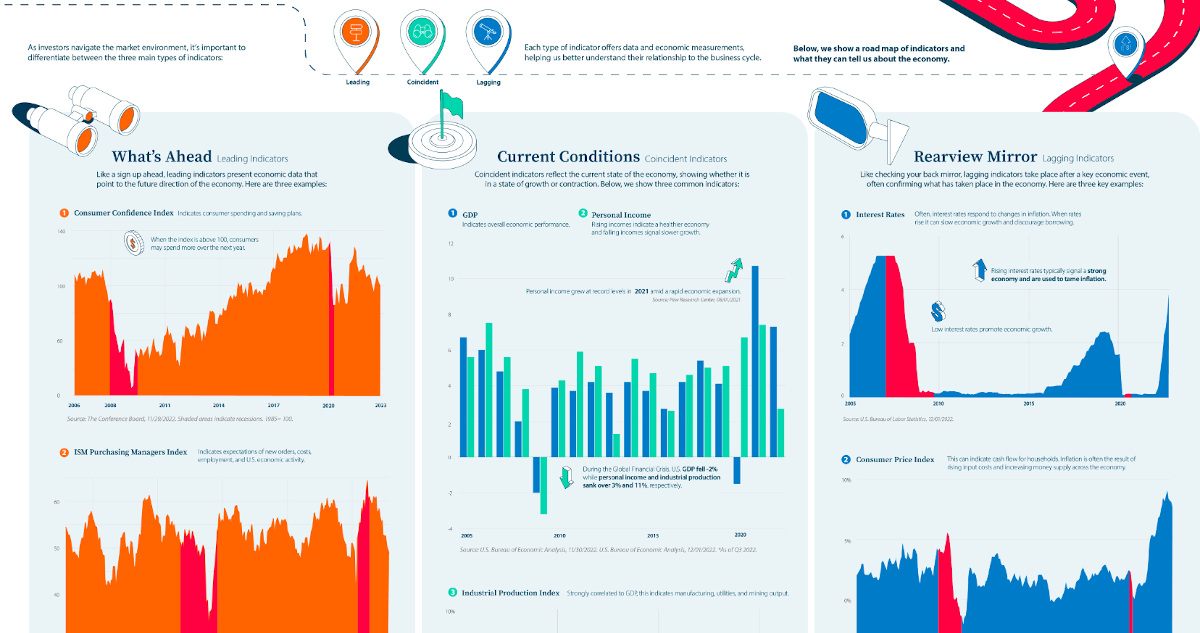

Visual Guide: The Three Types of Economic Indicators

From GDP to interest rates, this infographic shows key economic indicators for navigating the massive U.S. economy.

View the high resolution version of this infographic. Buy the poster.

A Visual Guide to Economic Indicators

Economic indicators provide insight on the state of financial markets.

Each type of indicator offers data and economic measurements, helping us better understand their relationship to the business cycle. As investors navigate the market environment, it’s important to differentiate between the three main types of indicators:

- Leading

- Coincident

- Lagging

The above infographic from New York Life Investments shows a road map of indicators and what they can tell us about the economy.

What’s Ahead: Leading Indicators

Leading indicators present economic data that point to the future direction of the economy like a sign up ahead. Here are three examples.

1. Consumer Confidence Index

This key measure indicates consumer spending and saving plans. When the index is above 100, consumers may spend more over the next year. In December, the index jumped to 108 up from 101 in November. This was in part due to lower inflation expectations and improving job prospects.

In the December survey, 48% indicated that the job market remained strong, highlighting the strength of employment opportunities and likely influencing sentiment towards spending in the future.

2. ISM Purchasing Managers Index

The ISM Purchasing Managers Index indicates expectations of new orders, costs, employment, and U.S. economic activity in the manufacturing sector. The following table shows how the index is broken down based on select measures:

| Index | Nov 2022 | Oct 2022 | Percentage Point Change | Direction | Trend (Months) |

|---|---|---|---|---|---|

| Manufacturing PMI | 49.0 | 50.2 | -1.2 | Contracting | 1 |

| New Orders | 47.2 | 49.2 | -2.0 | Contracting | 3 |

| Employment | 48.4 | 50.0 | -1.6 | Contracting | 1 |

| Prices | 43.0 | 46.6 | -3.6 | Decreasing | 2 |

| Imports | 46.6 | 50.8 | -4.2 | Contracting | 1 |

| Manufacturing Sector | Contracting | 1 |

For instance, in November the index fell into its first month of contraction since May 2020. Falling new orders signal that demand has weakened while contracting employment figures indicate lower output across the sector.

3. S&P 500 Index

The S&P 500 Index indicates the economy’s direction since forward-looking performance is factored into prices. In this way, the S&P 500 Index can represent investor confidence as the index often serves as a proxy for U.S. equity markets. In 2022, returns for the index are roughly -20% year-to-date.

Current Conditions: Coincident Indicators

Coincident indicators reflect the current state of the economy, showing whether it is in a state of growth or contraction.

1. GDP

GDP indicates overall economic performance. Typically it serves as the most comprehensive gauge of the economy since it tracks output across all sectors. In the third quarter of 2022, real U.S. GDP increased 2.9% on an annual basis. That compares to 2.7% for the same period in 2021.

2. Personal Income

Rising incomes indicate a healthier economy and falling incomes signal slower growth. Personal income grew at record levels in 2021 to 7.4% annually amid a rapid economic expansion.

This year, U.S. personal income has grown at a slower pace, at 2.7% on an annual basis as of the third quarter.

3. Industrial Production Index

Strongly correlated to GDP, the industrial production index indicates manufacturing, utilities, and mining output. Below, we show trends in industrial production and how they correspond with GDP and personal income indicators.

| Date | U.S. GDP | Personal Income | Industrial Production |

|---|---|---|---|

| 2022* | 7.3% | 2.7% | 4.7% |

| 2021 | 10.7% | 7.4% | 4.9% |

| 2020 | -1.5% | 6.7% | -7.0% |

| 2019 | 4.1% | 5.1% | -0.7% |

| 2018 | 5.4% | 5.0% | 3.2% |

| 2017 | 4.2% | 4.6% | 1.4% |

| 2016 | 2.7% | 2.6% | -2.0% |

| 2015 | 3.7% | 4.7% | -1.4% |

| 2014 | 4.2% | 5.5% | 3.0% |

| 2013 | 3.6% | 1.3% | 2.0% |

| 2012 | 4.2% | 5.1% | 3.0% |

| 2011 | 3.7% | 5.9% | 3.2% |

| 2010 | 3.9% | 4.3% | 5.5% |

| 2009 | -2.0% | -3.2% | -11.4% |

| 2008 | 2.0% | 3.8% | -3.5% |

| 2007 | 4.8% | 5.6% | 2.5% |

| 2006 | 6.0% | 7.5% | 2.3% |

| 2005 | 6.7% | 5.6% | 3.3% |

*As of Q3 2022.

As the above table shows, factory production collapsed following the 2008 financial crisis, a key indicator for the depth of an economic downturn. Meanwhile, personal income sank over -3% while GDP fell -2%.

Despite economic uncertainty in 2022, industrial production remains positive, at a 4.7% growth rate, albeit somewhat slower than 2021 levels.

Rearview Mirror: Lagging Indicators

Like checking your back mirror, lagging indicators take place after a key economic event, often confirming what has taken place in the economy. Here are three key examples.

1. Interest Rates

Often, interest rates respond to changes in inflation. When rates rise it can slow economic growth and discourage borrowing. Rising interest rates typically signal a strong economy and are used to tame inflation. On the other hand, low interest rates promote economic growth.

Following years of record-low interest rates, the Federal Funds rate increased at the fastest rate in decades over 2022, jumping from 0.25% in March to 4.25% in December as inflation accelerated.

2. Consumer Price Index

This inflation measure can indicate cash flow for households. Inflation is often the result of rising input costs and increasing money supply across the economy.

Sometimes, inflation can reach a peak after an expansion has ended as rising demand in an economy has pushed up prices. In November, U.S. inflation reached 7.1% annually amid supply chain disruptions and price pressures across food prices, medical prices, and housing costs.

| Year | Inflation Rate | Annual Change |

|---|---|---|

| 2022* | 7.1% | 2.4% |

| 2021 | 4.7% | 3.5% |

| 2020 | 1.2% | -0.6% |

| 2019 | 1.8% | -0.6% |

| 2018 | 2.4% | 0.3% |

| 2017 | 2.1% | 0.9% |

| 2016 | 1.3% | 1.1% |

| 2015 | 0.1% | -1.5% |

| 2014 | 1.6% | 0.2% |

| 2013 | 1.5% | -0.6% |

| 2012 | 2.1% | -1.1% |

| 2011 | 3.2% | 1.5% |

| 2010 | 1.6% | 2.0% |

| 2009 | -0.4% | -4.2% |

| 2008 | 3.8% | 1.0% |

| 2007 | 2.9% | -0.4% |

| 2006 | 3.2% | -0.2% |

| 2005 | 3.4% | 0.7% |

*As of November 2022.

3. Unemployment Rate

The unemployment rate has many spillover effects, impacting consumer spending and in turn retail sales and GDP. Historically, unemployment falls slowly after an economic recovery which is why it’s considered a lagging indicator. When the unemployment rate rises it confirms lagging economic performance.

Overall, 2022 has been characterized by a strong job market, with unemployment levels below historical averages, at 3.7% as of October.

On the Road

To get a more comprehensive picture of the economy, combining a number of indicators is more effective than isolating a few variables. With these tools, investors can gain more perspective on the cyclical nature of the business cycle while keeping a long-term perspective in mind on the road ahead.

The Top 5 Reasons Clients Fire a Financial Advisor

The Top 5 Reasons Clients Hire a Financial Advisor

Visualizing the Growth of $100, by Asset Class

How Small Investments Make a Big Impact Over Time

What Were the Top Performing Investment Themes of 2023?

-

Infographics2 years ago

Infographics2 years agoThe Top Investment Quotes Every Investor Should Know

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoMapped: The Growth in U.S. House Prices by State

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoHow Closely Related Are Historical Mortgage Rates and Housing Prices?

-

Infographics2 years ago

Infographics2 years agoA Visual Guide to Stagflation, Inflation, and Deflation

-

Markets in a Minute1 year ago

Markets in a Minute1 year agoMapped: Global Energy Prices, by Country in 2022

-

Infographics3 years ago

Infographics3 years agoThe 5 Fastest Growing Industries of the Next Decade

-

Markets in a Minute2 years ago

Markets in a Minute2 years agoVisualizing Historical Oil Prices (1968-2022)

-

Infographics1 year ago

Infographics1 year agoVisual Guide: The Three Types of Economic Indicators